- Saudi Arabia

- /

- Basic Materials

- /

- SASE:3091

Al Jouf Cement Company's (TADAWUL:3091) Shares Bounce 28% But Its Business Still Trails The Market

The Al Jouf Cement Company (TADAWUL:3091) share price has done very well over the last month, posting an excellent gain of 28%. Notwithstanding the latest gain, the annual share price return of 9.0% isn't as impressive.

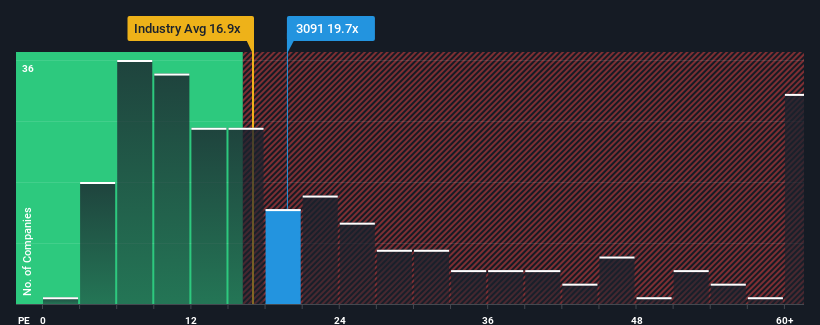

Even after such a large jump in price, Al Jouf Cement may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 19.7x, since almost half of all companies in Saudi Arabia have P/E ratios greater than 25x and even P/E's higher than 43x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Earnings have risen at a steady rate over the last year for Al Jouf Cement, which is generally not a bad outcome. It might be that many expect the respectable earnings performance to degrade, which has repressed the P/E. If that doesn't eventuate, then existing shareholders may have reason to be optimistic about the future direction of the share price.

See our latest analysis for Al Jouf Cement

Is There Any Growth For Al Jouf Cement?

The only time you'd be truly comfortable seeing a P/E as low as Al Jouf Cement's is when the company's growth is on track to lag the market.

If we review the last year of earnings growth, the company posted a worthy increase of 5.5%. Still, EPS has barely risen at all in aggregate from three years ago, which is not ideal. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

This is in contrast to the rest of the market, which is expected to grow by 15% over the next year, materially higher than the company's recent medium-term annualised growth rates.

With this information, we can see why Al Jouf Cement is trading at a P/E lower than the market. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

The Key Takeaway

The latest share price surge wasn't enough to lift Al Jouf Cement's P/E close to the market median. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Al Jouf Cement maintains its low P/E on the weakness of its recent three-year growth being lower than the wider market forecast, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 2 warning signs for Al Jouf Cement (1 is concerning!) that we have uncovered.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:3091

Al Jouf Cement

Engages in production and sale of cement in the Kingdom of Saudi Arabia.

Imperfect balance sheet very low.