Advertisement

- Saudi Arabia

- /

- Basic Materials

- /

- SASE:3080

Eastern Province Cement Co.'s (TADAWUL:3080) Has Been On A Rise But Financial Prospects Look Weak: Is The Stock Overpriced?

Eastern Province Cement (TADAWUL:3080) has had a great run on the share market with its stock up by a significant 14% over the last three months. We, however wanted to have a closer look at its key financial indicators as the markets usually pay for long-term fundamentals, and in this case, they don't look very promising. Specifically, we decided to study Eastern Province Cement's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

See our latest analysis for Eastern Province Cement

How To Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Eastern Province Cement is:

9.2% = ر.س225m ÷ ر.س2.4b (Based on the trailing twelve months to September 2020).

The 'return' is the profit over the last twelve months. So, this means that for every SAR1 of its shareholder's investments, the company generates a profit of SAR0.09.

What Has ROE Got To Do With Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Eastern Province Cement's Earnings Growth And 9.2% ROE

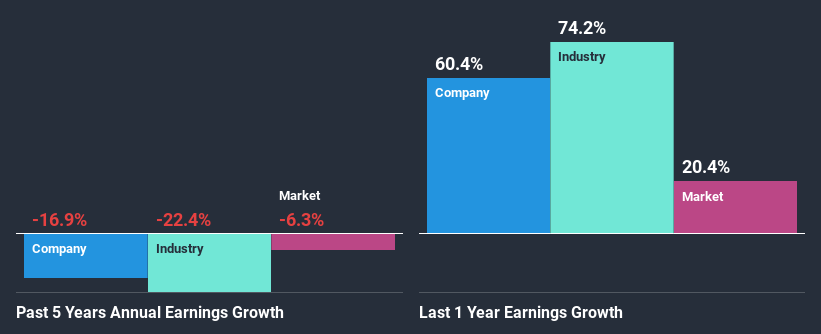

It is hard to argue that Eastern Province Cement's ROE is much good in and of itself. Further, we noted that the company's ROE is similar to the industry average of 9.1%. Therefore, it might not be wrong to say that the five year net income decline of 17% seen by Eastern Province Cement was possibly a result of the disappointing ROE.

Next, we compared Eastern Province Cement's performance against the industry and found that the industry shrunk its earnings at 22% in the same period, which suggests that the company's earnings have been shrinking at a slower rate than its industry, This does offer shareholders some relief

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. Is Eastern Province Cement fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Eastern Province Cement Efficiently Re-investing Its Profits?

Eastern Province Cement's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 71% (or a retention ratio of 29%). With only very little left to reinvest into the business, growth in earnings is far from likely. Our risks dashboard should have the 2 risks we have identified for Eastern Province Cement.

Moreover, Eastern Province Cement has been paying dividends for nine years, which is a considerable amount of time, suggesting that management must have perceived that the shareholders prefer consistent dividends even though earnings have been shrinking. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 78%. Therefore, the company's future ROE is also not expected to change by much with analysts predicting an ROE of 7.7%.

Summary

Overall, we would be extremely cautious before making any decision on Eastern Province Cement. The company has seen a lack of earnings growth as a result of retaining very little profits and whatever little it does retain, is being reinvested at a very low rate of return. That being so, the latest industry analyst forecasts show that analysts are forecasting a slight improvement in the company's future earnings growth. The company's existing shareholders might have some respite after all. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

If you decide to trade Eastern Province Cement, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Eastern Province Cement might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SASE:3080

Eastern Province Cement

Produces and sells clinker and cement in the Kingdom of Saudi Arabia and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor