- Saudi Arabia

- /

- Chemicals

- /

- SASE:2290

Yanbu National Petrochemical Company's (TADAWUL:2290) Shares May Have Run Too Fast Too Soon

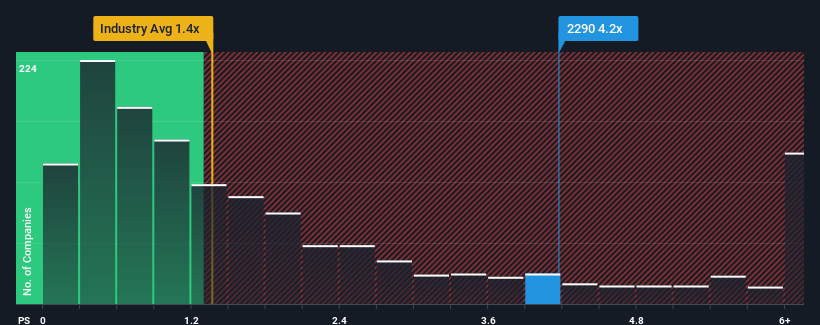

When you see that almost half of the companies in the Chemicals industry in Saudi Arabia have price-to-sales ratios (or "P/S") below 1.9x, Yanbu National Petrochemical Company (TADAWUL:2290) looks to be giving off strong sell signals with its 4.2x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

View our latest analysis for Yanbu National Petrochemical

How Yanbu National Petrochemical Has Been Performing

With only a limited decrease in revenue compared to most other companies of late, Yanbu National Petrochemical has been doing relatively well. Perhaps the market is expecting the company to continue to outperform the industry, which has propped up the P/S. If not, then existing shareholders might be a little nervous about the viability of the share price, especially if revenue continues to dissolve.

Want the full picture on analyst estimates for the company? Then our free report on Yanbu National Petrochemical will help you uncover what's on the horizon.How Is Yanbu National Petrochemical's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as Yanbu National Petrochemical's is when the company's growth is on track to outshine the industry decidedly.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 8.0%. This means it has also seen a slide in revenue over the longer-term as revenue is down 5.5% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to climb by 12% per annum during the coming three years according to the eleven analysts following the company. With the industry predicted to deliver 9.7% growth per annum, the company is positioned for a comparable revenue result.

With this information, we find it interesting that Yanbu National Petrochemical is trading at a high P/S compared to the industry. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for disappointment if the P/S falls to levels more in line with the growth outlook.

What We Can Learn From Yanbu National Petrochemical's P/S?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Seeing as its revenues are forecast to grow in line with the wider industry, it would appear that Yanbu National Petrochemical currently trades on a higher than expected P/S. The fact that the revenue figures aren't setting the world alight has us doubtful that the company's elevated P/S can be sustainable for the long term. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Having said that, be aware Yanbu National Petrochemical is showing 1 warning sign in our investment analysis, you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SASE:2290

Yanbu National Petrochemical

Engages in the manufacture and sale of petrochemical products in Saudi Arabia, the Americas, Africa, the Middle East, Europe, and Asia.

Flawless balance sheet with reasonable growth potential.

Market Insights

Community Narratives