Advertisement

- Saudi Arabia

- /

- Chemicals

- /

- SASE:2290

Yanbu National Petrochemical Company (TADAWUL:2290) Investors Are Less Pessimistic Than Expected

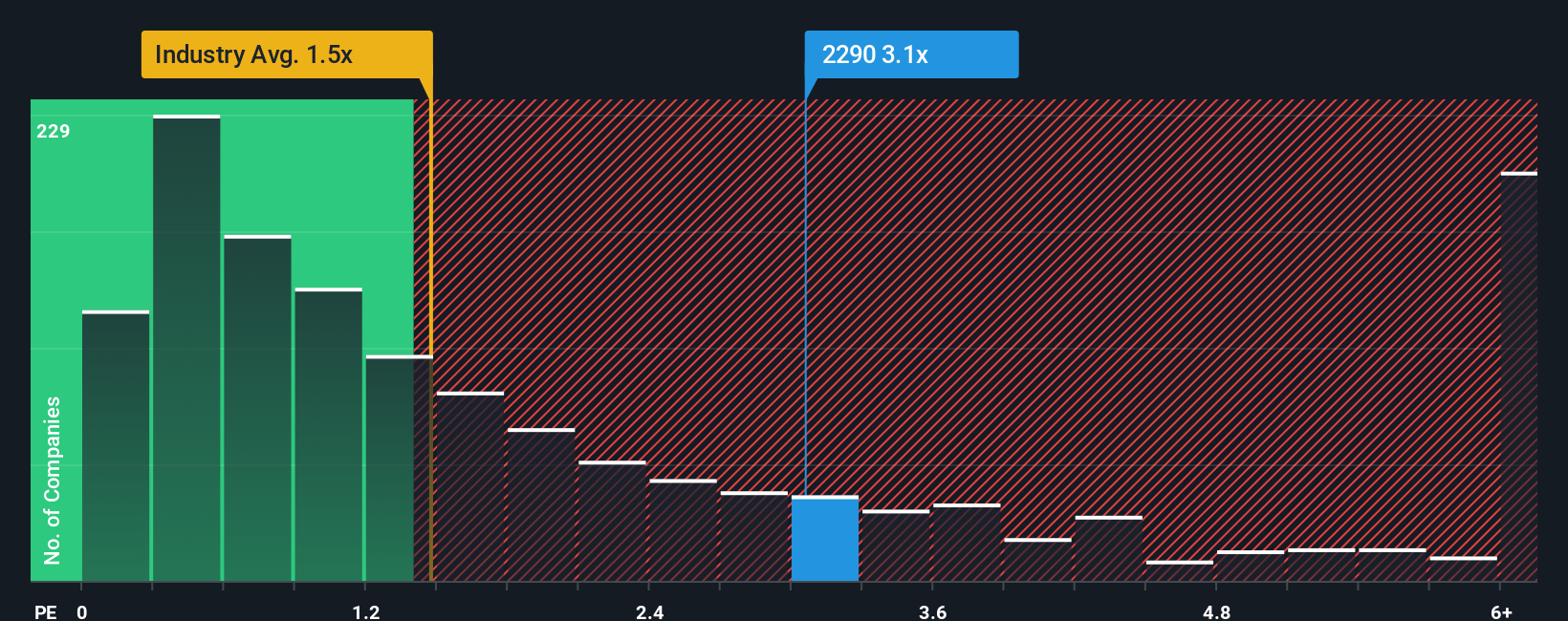

When you see that almost half of the companies in the Chemicals industry in Saudi Arabia have price-to-sales ratios (or "P/S") below 1.6x, Yanbu National Petrochemical Company (TADAWUL:2290) looks to be giving off some sell signals with its 3.1x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Yanbu National Petrochemical

What Does Yanbu National Petrochemical's Recent Performance Look Like?

Yanbu National Petrochemical certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Yanbu National Petrochemical.Do Revenue Forecasts Match The High P/S Ratio?

Yanbu National Petrochemical's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Retrospectively, the last year delivered a decent 7.7% gain to the company's revenues. Still, lamentably revenue has fallen 23% in aggregate from three years ago, which is disappointing. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 3.1% each year as estimated by the seven analysts watching the company. With the industry predicted to deliver 3.0% growth per annum, the company is positioned for a comparable revenue result.

With this information, we find it interesting that Yanbu National Petrochemical is trading at a high P/S compared to the industry. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of revenue growth is likely to weigh down the share price eventually.

The Key Takeaway

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Analysts are forecasting Yanbu National Petrochemical's revenues to only grow on par with the rest of the industry, which has lead to the high P/S ratio being unexpected. When we see revenue growth that just matches the industry, we don't expect elevates P/S figures to remain inflated for the long-term. A positive change is needed in order to justify the current price-to-sales ratio.

Before you settle on your opinion, we've discovered 1 warning sign for Yanbu National Petrochemical that you should be aware of.

If you're unsure about the strength of Yanbu National Petrochemical's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:2290

Yanbu National Petrochemical

Manufactures and sells petrochemical products in the Kingdom of Saudi Arabia, the United States, Africa, the Middle East, Europe, and Asia.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.9% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.9% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|64.1% undervalued

ME

Community Contributor