Advertisement

- Saudi Arabia

- /

- Insurance

- /

- SASE:8300

Even With A 27% Surge, Cautious Investors Are Not Rewarding Wataniya Insurance Company's (TADAWUL:8300) Performance Completely

Despite an already strong run, Wataniya Insurance Company (TADAWUL:8300) shares have been powering on, with a gain of 27% in the last thirty days. Looking back a bit further, it's encouraging to see the stock is up 55% in the last year.

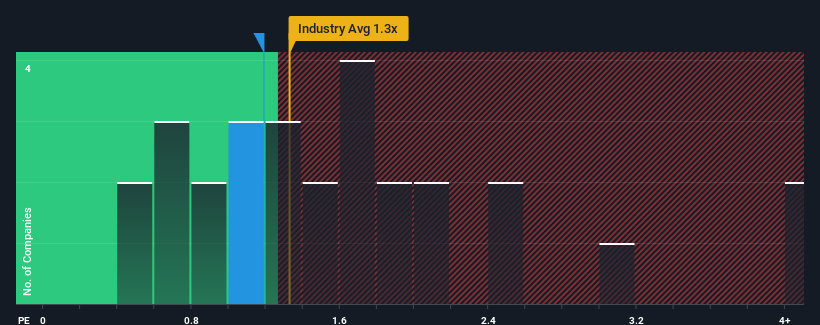

In spite of the firm bounce in price, it's still not a stretch to say that Wataniya Insurance's price-to-sales (or "P/S") ratio of 1.2x right now seems quite "middle-of-the-road" compared to the Insurance industry in Saudi Arabia, where the median P/S ratio is around 1.3x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for Wataniya Insurance

How Has Wataniya Insurance Performed Recently?

Recent times have been quite advantageous for Wataniya Insurance as its revenue has been rising very briskly. Perhaps the market is expecting future revenue performance to taper off, which has kept the P/S from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Wataniya Insurance's earnings, revenue and cash flow.Is There Some Revenue Growth Forecasted For Wataniya Insurance?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Wataniya Insurance's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 46% last year. The latest three year period has also seen an excellent 72% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Weighing the recent medium-term upward revenue trajectory against the broader industry's one-year forecast for contraction of 1.2% shows it's a great look while it lasts.

With this in mind, we find it intriguing that Wataniya Insurance's P/S matches its industry peers. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

What We Can Learn From Wataniya Insurance's P/S?

Wataniya Insurance appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Wataniya Insurance revealed its growing revenue over the medium-term hasn't helped elevate its P/S above that of the industry, which is surprising given the industry is set to shrink. There could be some unobserved threats to revenue preventing the P/S ratio from outpacing the industry much like its revenue performance. Perhaps there is some hesitation about the company's ability to stay its recent course and swim against the current of the broader industry turmoil. The fact that the company's relative performance has not provided a kick to the share price suggests that some investors are anticipating revenue instability.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Wataniya Insurance, and understanding should be part of your investment process.

If these risks are making you reconsider your opinion on Wataniya Insurance, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Wataniya Insurance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:8300

Wataniya Insurance

Provides a range of insurance products and services in the Kingdom of Saudi Arabia.

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.9% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor