- Saudi Arabia

- /

- Insurance

- /

- SASE:8270

Why Investors Shouldn't Be Surprised By Buruj Cooperative Insurance Company's (TADAWUL:8270) 25% Share Price Surge

Buruj Cooperative Insurance Company (TADAWUL:8270) shareholders would be excited to see that the share price has had a great month, posting a 25% gain and recovering from prior weakness. Notwithstanding the latest gain, the annual share price return of 2.5% isn't as impressive.

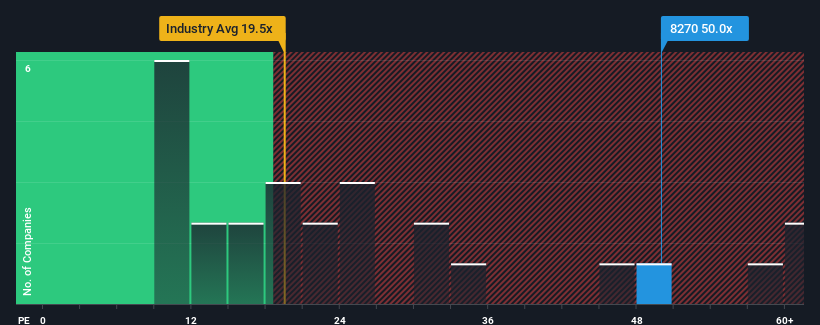

Since its price has surged higher, given close to half the companies in Saudi Arabia have price-to-earnings ratios (or "P/E's") below 23x, you may consider Buruj Cooperative Insurance as a stock to avoid entirely with its 50x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

As an illustration, earnings have deteriorated at Buruj Cooperative Insurance over the last year, which is not ideal at all. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

View our latest analysis for Buruj Cooperative Insurance

Is There Enough Growth For Buruj Cooperative Insurance?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Buruj Cooperative Insurance's to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 23%. However, a few very strong years before that means that it was still able to grow EPS by an impressive 113% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 16% shows it's noticeably more attractive on an annualised basis.

In light of this, it's understandable that Buruj Cooperative Insurance's P/E sits above the majority of other companies. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

The Final Word

The strong share price surge has got Buruj Cooperative Insurance's P/E rushing to great heights as well. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Buruj Cooperative Insurance maintains its high P/E on the strength of its recent three-year growth being higher than the wider market forecast, as expected. Right now shareholders are comfortable with the P/E as they are quite confident earnings aren't under threat. If recent medium-term earnings trends continue, it's hard to see the share price falling strongly in the near future under these circumstances.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with Buruj Cooperative Insurance, and understanding should be part of your investment process.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Buruj Cooperative Insurance might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:8270

Buruj Cooperative Insurance

Provides various general insurance products to individuals and business customers in the Kingdom of Saudi Arabia.

Flawless balance sheet with poor track record.

Market Insights

Community Narratives