- Saudi Arabia

- /

- Healthcare Services

- /

- SASE:4013

Dr. Sulaiman Al Habib Medical Services Group (TADAWUL:4013) Posted Healthy Earnings But There Are Some Other Factors To Be Aware Of

Dr. Sulaiman Al Habib Medical Services Group Company (TADAWUL:4013) announced strong profits, but the stock was stagnant. Our analysis suggests that shareholders have noticed something concerning in the numbers.

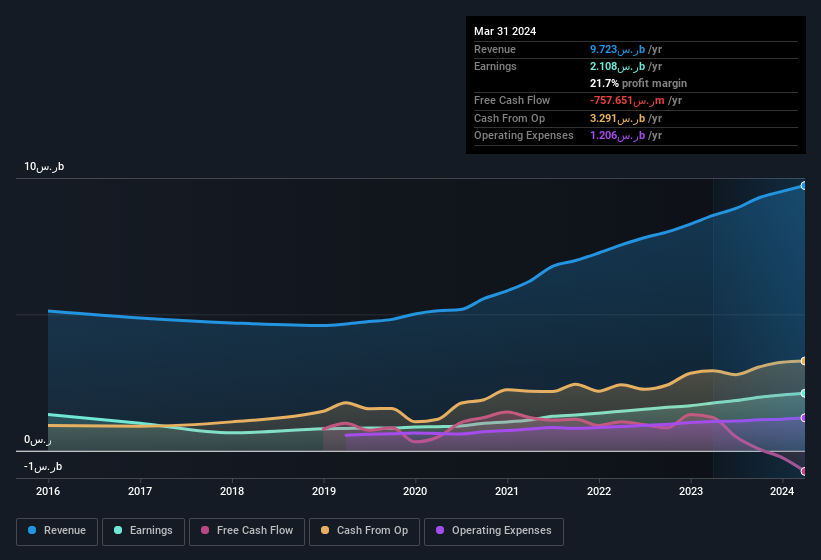

View our latest analysis for Dr. Sulaiman Al Habib Medical Services Group

Zooming In On Dr. Sulaiman Al Habib Medical Services Group's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

Dr. Sulaiman Al Habib Medical Services Group has an accrual ratio of 0.34 for the year to March 2024. Unfortunately, that means its free cash flow was a lot less than its statutory profit, which makes us doubt the utility of profit as a guide. Even though it reported a profit of ر.س2.11b, a look at free cash flow indicates it actually burnt through ر.س758m in the last year. It's worth noting that Dr. Sulaiman Al Habib Medical Services Group generated positive FCF of ر.س1.2b a year ago, so at least they've done it in the past.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Dr. Sulaiman Al Habib Medical Services Group's Profit Performance

As we discussed above, we think Dr. Sulaiman Al Habib Medical Services Group's earnings were not supported by free cash flow, which might concern some investors. For this reason, we think that Dr. Sulaiman Al Habib Medical Services Group's statutory profits may be a bad guide to its underlying earnings power, and might give investors an overly positive impression of the company. But on the bright side, its earnings per share have grown at an extremely impressive rate over the last three years. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. When we did our research, we found 2 warning signs for Dr. Sulaiman Al Habib Medical Services Group (1 is concerning!) that we believe deserve your full attention.

Today we've zoomed in on a single data point to better understand the nature of Dr. Sulaiman Al Habib Medical Services Group's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SASE:4013

Dr. Sulaiman Al Habib Medical Services Group

Dr. Sulaiman Al Habib Medical Services Group Company establishes, manages, and operates hospitals, general and specialized medical complexes, day surgery centers, and pharmaceutical facilities in Saudi Arabia and internationally.

Moderate growth potential with acceptable track record.