Advertisement

- Italy

- /

- Construction

- /

- BIT:ICOP

European Market's Estimated Value Opportunities For February 2025

Simply Wall St

Reviewed by Simply Wall St

As February 2025 unfolds, the European markets are navigating a landscape marked by cautious optimism amidst geopolitical tensions and evolving trade policies. Despite mixed performances in major indices like Germany's DAX and France's CAC 40, investors remain attentive to value opportunities that may arise from current economic conditions. Identifying undervalued stocks requires a keen eye on factors such as business activity levels, inflation trends, and sector-specific developments that could signal potential for growth or resilience in this complex environment.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Sword Group (ENXTPA:SWP) | €33.30 | €64.76 | 48.6% |

| Vestas Wind Systems (CPSE:VWS) | DKK102.35 | DKK204.12 | 49.9% |

| Laboratorio Reig Jofre (BME:RJF) | €2.69 | €5.32 | 49.4% |

| Star7 (BIT:STAR7) | €6.40 | €12.38 | 48.3% |

| Cint Group (OM:CINT) | SEK6.745 | SEK13.29 | 49.2% |

| Surgical Science Sweden (OM:SUS) | SEK157.50 | SEK310.06 | 49.2% |

| Canatu Oyj (HLSE:CANATU) | €12.80 | €24.82 | 48.4% |

| Better Collective (OM:BETCO) | SEK109.20 | SEK216.56 | 49.6% |

| Fodelia Oyj (HLSE:FODELIA) | €7.20 | €13.91 | 48.2% |

| Galderma Group (SWX:GALD) | CHF109.48 | CHF212.91 | 48.6% |

Let's explore several standout options from the results in the screener.

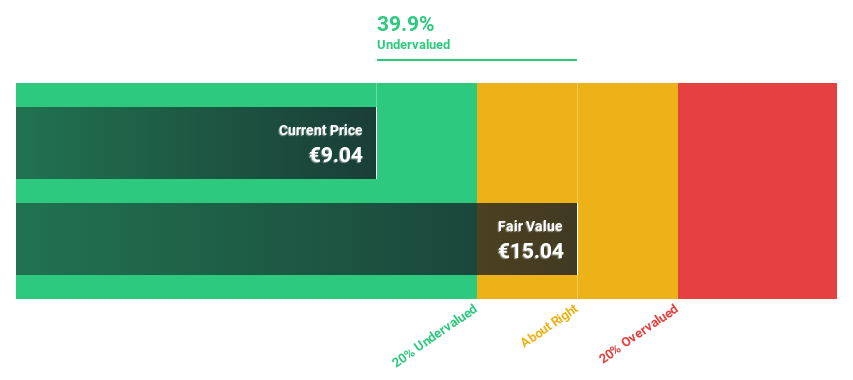

I.CO.P.. Società Benefit (BIT:ICOP)

Overview: I.CO.P. S.p.A. Società Benefit offers construction and special engineering services to both public and private clients in Italy and abroad, with a market cap of €260.87 million.

Operations: The company generates revenue of €117.92 million from its heavy construction segment, serving both domestic and international markets.

Estimated Discount To Fair Value: 37.4%

I.CO.P. Società Benefit is currently trading at €9.44, significantly below its estimated fair value of €15.07, presenting a potential undervaluation based on cash flows. With earnings forecasted to grow 56.26% annually and revenue expected to increase by 48.4% per year, the company shows strong growth prospects compared to the Italian market averages. However, interest payments are not well covered by earnings and financial data may be outdated, warranting cautious consideration for investors seeking undervalued opportunities in Europe.

- Our earnings growth report unveils the potential for significant increases in I.CO.P.. Società Benefit's future results.

- Dive into the specifics of I.CO.P.. Società Benefit here with our thorough financial health report.

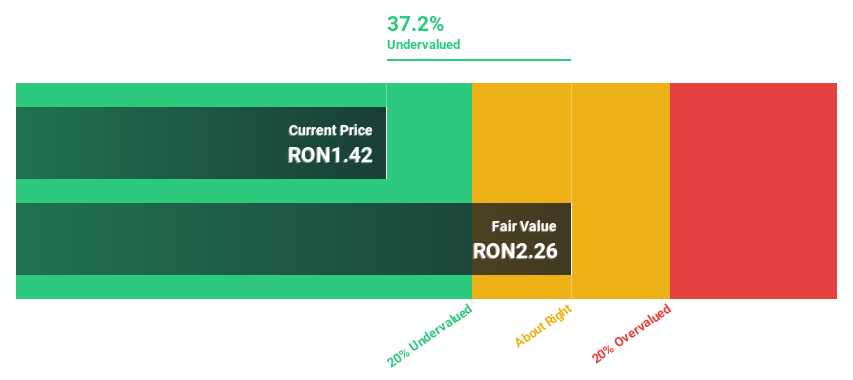

Aquila Part Prod Com (BVB:AQ)

Overview: Aquila Part Prod Com S.A. offers integrated distribution and logistics services across Romania, Moldova, Germany, the Netherlands, and other international markets with a market cap of RON1.72 billion.

Operations: The company's revenue is primarily derived from its distribution segment, which accounts for RON2.70 billion, complemented by logistics and transport segments generating RON92.36 million and RON64.22 million, respectively.

Estimated Discount To Fair Value: 36.5%

Aquila Part Prod Com is trading at RON1.43, significantly below its estimated fair value of RON2.25, suggesting potential undervaluation based on cash flows. Earnings are expected to grow 21.8% annually, outpacing the Romanian market's 2.3% growth forecast, while revenue is projected to rise by 12.4% per year. However, the dividend yield of 4.95% lacks coverage by earnings or free cash flows, indicating sustainability concerns for income-focused investors.

- According our earnings growth report, there's an indication that Aquila Part Prod Com might be ready to expand.

- Click here to discover the nuances of Aquila Part Prod Com with our detailed financial health report.

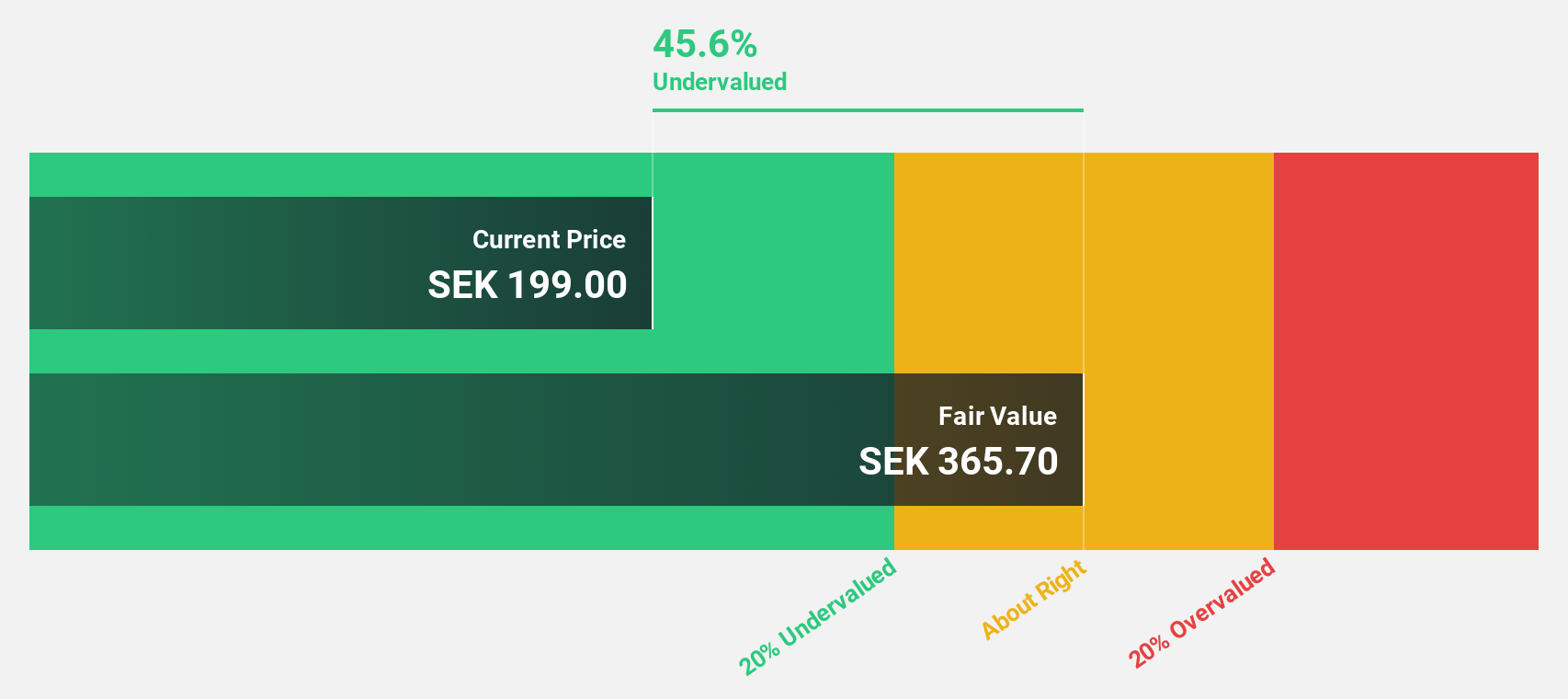

Lindab International (OM:LIAB)

Overview: Lindab International AB (publ) is a European manufacturer and seller of products and solutions for ventilation systems, with a market cap of SEK15.72 billion.

Operations: Lindab International derives its revenue from two main segments: Ventilation Systems, contributing SEK10.21 billion, and Profile Systems, accounting for SEK3.12 billion.

Estimated Discount To Fair Value: 45.2%

Lindab International is trading at SEK204, substantially below its estimated fair value of SEK372.27, highlighting potential undervaluation based on cash flows. Earnings are forecast to grow significantly at 38.6% annually, surpassing the Swedish market's 9.5% growth rate; however, recent profit margins have declined to 2.4%. Despite a proposed dividend of SEK5.40 per share, coverage by earnings remains inadequate. Lindab's commitment to sustainability is underscored by linking its credit facility to ambitious environmental targets.

- Insights from our recent growth report point to a promising forecast for Lindab International's business outlook.

- Navigate through the intricacies of Lindab International with our comprehensive financial health report here.

Where To Now?

- Embark on your investment journey to our 197 Undervalued European Stocks Based On Cash Flows selection here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:ICOP

I.CO.P.. Società Benefit

Engages in providing construction and special engineering services to public and private clients in Italy and internationally.

Exceptional growth potential with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.6% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.3% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|87.8% undervalued

AG

Community Contributor