Advertisement

- Poland

- /

- Capital Markets

- /

- WSE:LUD

Rock star Growth Puts FinTech Ventures (WSE:FIV) In A Position To Use Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, FinTech Ventures S.A. (WSE:FIV) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for FinTech Ventures

What Is FinTech Ventures's Net Debt?

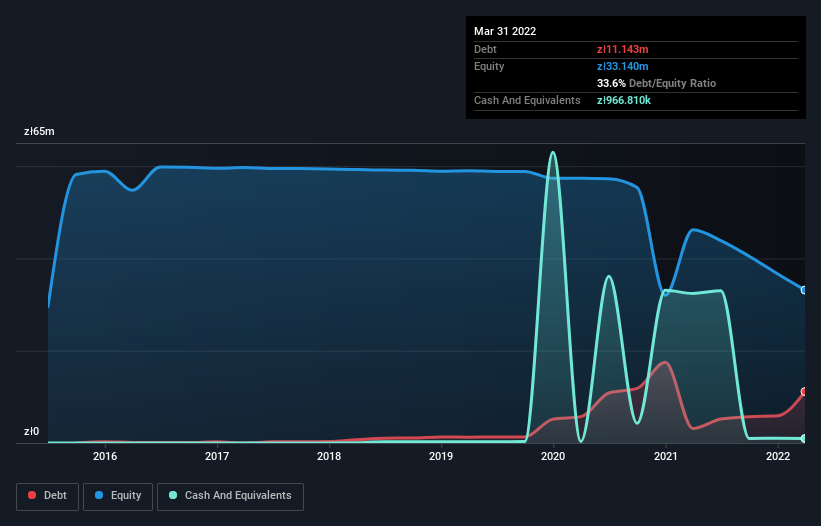

The image below, which you can click on for greater detail, shows that at March 2022 FinTech Ventures had debt of zł11.1m, up from zł3.13m in one year. However, because it has a cash reserve of zł966.8k, its net debt is less, at about zł10.2m.

A Look At FinTech Ventures' Liabilities

According to the balance sheet data, FinTech Ventures had liabilities of zł14.5m due within 12 months, but no longer term liabilities. Offsetting these obligations, it had cash of zł966.8k as well as receivables valued at zł31.4m due within 12 months. So it actually has zł17.8m more liquid assets than total liabilities.

This luscious liquidity implies that FinTech Ventures' balance sheet is sturdy like a giant sequoia tree. Having regard to this fact, we think its balance sheet is as strong as an ox. There's no doubt that we learn most about debt from the balance sheet. But it is FinTech Ventures's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, FinTech Ventures reported revenue of zł2.1m, which is a gain of 69%, although it did not report any earnings before interest and tax. Shareholders probably have their fingers crossed that it can grow its way to profits.

Caveat Emptor

While we can certainly appreciate FinTech Ventures's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. Its EBIT loss was a whopping zł10m. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. Still, we'd be more encouraged to study the business in depth if it already had some free cash flow. So it seems too risky for our taste. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 6 warning signs for FinTech Ventures (of which 3 make us uncomfortable!) you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:LUD

Ludus

Operates an esports platform. The company provides services, such as e-wallet; courses, masterclasses, and private coaching; deals solutions; cashback; FIFA; fitness tracker; marketplace for NFTs; greets that allows communication; and banking solutions.

Adequate balance sheet low.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor