- Poland

- /

- Life Sciences

- /

- WSE:RVU

Despite Lacking Profits Ryvu Therapeutics (WSE:RVU) Seems To Be On Top Of Its Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Ryvu Therapeutics S.A. (WSE:RVU) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Ryvu Therapeutics

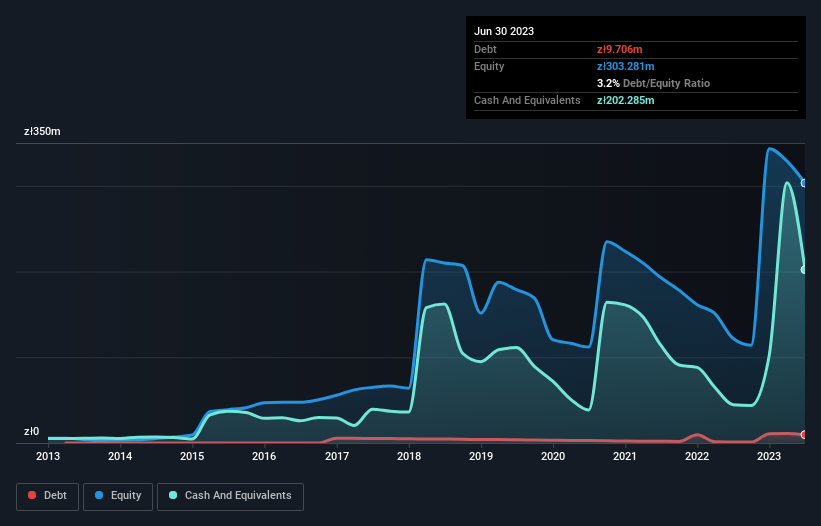

What Is Ryvu Therapeutics's Debt?

You can click the graphic below for the historical numbers, but it shows that as of June 2023 Ryvu Therapeutics had zł9.71m of debt, an increase on zł1.23m, over one year. But it also has zł202.3m in cash to offset that, meaning it has zł192.6m net cash.

How Strong Is Ryvu Therapeutics' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Ryvu Therapeutics had liabilities of zł58.4m due within 12 months and liabilities of zł63.5m due beyond that. Offsetting these obligations, it had cash of zł202.3m as well as receivables valued at zł28.0m due within 12 months. So it can boast zł108.4m more liquid assets than total liabilities.

This surplus suggests that Ryvu Therapeutics has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, Ryvu Therapeutics boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Ryvu Therapeutics can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Ryvu Therapeutics reported revenue of zł88m, which is a gain of 134%, although it did not report any earnings before interest and tax. So there's no doubt that shareholders are cheering for growth

So How Risky Is Ryvu Therapeutics?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Ryvu Therapeutics lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of zł1.9m and booked a zł66m accounting loss. With only zł192.6m on the balance sheet, it would appear that its going to need to raise capital again soon. The good news for shareholders is that Ryvu Therapeutics has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Ryvu Therapeutics is showing 3 warning signs in our investment analysis , and 1 of those is a bit concerning...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:RVU

Ryvu Therapeutics

A clinical-stage drug discovery and development company, engages in developing of small molecule therapies for treatment in oncology in Poland, European Union, and internationally.

Excellent balance sheet very low.

Market Insights

Community Narratives