- Poland

- /

- Interactive Media and Services

- /

- WSE:WPL

Here's Why Wirtualna Polska Holding (WSE:WPL) Can Manage Its Debt Responsibly

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Wirtualna Polska Holding S.A. (WSE:WPL) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Wirtualna Polska Holding

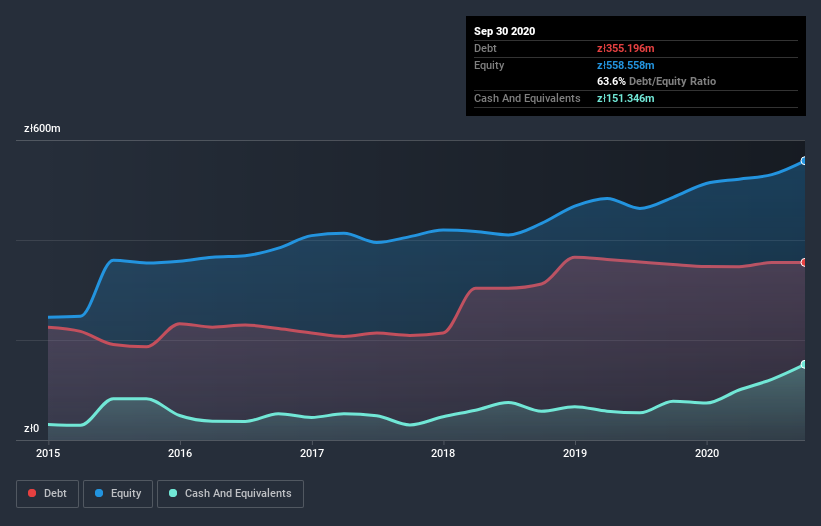

How Much Debt Does Wirtualna Polska Holding Carry?

As you can see below, Wirtualna Polska Holding had zł355.2m of debt, at September 2020, which is about the same as the year before. You can click the chart for greater detail. However, it does have zł151.3m in cash offsetting this, leading to net debt of about zł203.9m.

A Look At Wirtualna Polska Holding's Liabilities

The latest balance sheet data shows that Wirtualna Polska Holding had liabilities of zł184.4m due within a year, and liabilities of zł447.0m falling due after that. Offsetting this, it had zł151.3m in cash and zł129.1m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by zł351.0m.

Given Wirtualna Polska Holding has a market capitalization of zł2.58b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

With net debt sitting at just 1.1 times EBITDA, Wirtualna Polska Holding is arguably pretty conservatively geared. And this view is supported by the solid interest coverage, with EBIT coming in at 8.4 times the interest expense over the last year. Wirtualna Polska Holding's EBIT was pretty flat over the last year, but that shouldn't be an issue given the it doesn't have a lot of debt. When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Wirtualna Polska Holding's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Wirtualna Polska Holding actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Our View

Wirtualna Polska Holding's conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. And its interest cover is good too. When we consider the range of factors above, it looks like Wirtualna Polska Holding is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 1 warning sign for Wirtualna Polska Holding that you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

When trading Wirtualna Polska Holding or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Wirtualna Polska Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About WSE:WPL

Wirtualna Polska Holding

Through its subsidiaries, engages in the media, advertising, and e-commerce businesses in Poland.

Undervalued with moderate growth potential.