Today is shaping up negative for CD Projekt S.A. (WSE:CDR) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting analysts have soured majorly on the business.

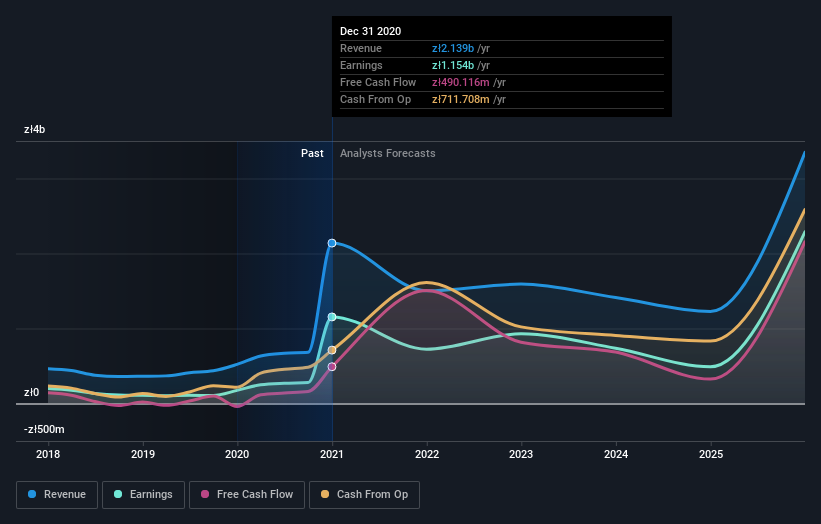

Following the latest downgrade, the current consensus, from the 17 analysts covering CD Projekt, is for revenues of zł1.6b in 2021, which would reflect a disturbing 25% reduction in CD Projekt's sales over the past 12 months. Statutory earnings per share are supposed to plunge 31% to zł8.21 in the same period. Prior to this update, the analysts had been forecasting revenues of zł1.9b and earnings per share (EPS) of zł11.30 in 2021. It looks like analyst sentiment has declined substantially, with a measurable cut to revenue estimates and a pretty serious decline to earnings per share numbers as well.

Check out our latest analysis for CD Projekt

It'll come as no surprise then, to learn that the analysts have cut their price target 5.5% to zł238. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values CD Projekt at zł448 per share, while the most bearish prices it at zł100.00. As you can see the range of estimates is wide, with the lowest valuation coming in at less than half the most bullish estimate, suggesting there are some strongly diverging views on how think this business will perform. As a result it might not be possible to derive much meaning from the consensus price target, which is after all just an average of this wide range of estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the CD Projekt's past performance and to peers in the same industry. We would highlight that sales are expected to reverse, with a forecast 25% annualised revenue decline to the end of 2021. That is a notable change from historical growth of 8.7% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 13% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - CD Projekt is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

As you can see, the analysts clearly aren't bullish, and there might be good reason for that. We've identified some potential issues with CD Projekt's financials, such as concerns around earnings quality. Learn more, and discover the 3 other concerns we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

When trading CD Projekt or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About WSE:CDR

CD Projekt

Together its subsidiaries, engages in the development, publishing, and digital distribution of video games for personal computers and video game consoles in Poland.

Exceptional growth potential with flawless balance sheet.