Investors Could Be Concerned With Polwax's (WSE:PWX) Returns On Capital

What financial metrics can indicate to us that a company is maturing or even in decline? Typically, we'll see the trend of both return on capital employed (ROCE) declining and this usually coincides with a decreasing amount of capital employed. Ultimately this means that the company is earning less per dollar invested and on top of that, it's shrinking its base of capital employed. In light of that, from a first glance at Polwax (WSE:PWX), we've spotted some signs that it could be struggling, so let's investigate.

Return On Capital Employed (ROCE): What is it?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Polwax:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

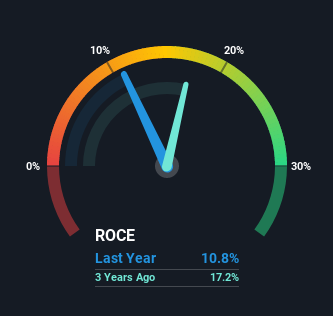

0.11 = zł10m ÷ (zł201m - zł107m) (Based on the trailing twelve months to September 2021).

Therefore, Polwax has an ROCE of 11%. On its own, that's a standard return, however it's much better than the 7.7% generated by the Chemicals industry.

View our latest analysis for Polwax

Historical performance is a great place to start when researching a stock so above you can see the gauge for Polwax's ROCE against it's prior returns. If you'd like to look at how Polwax has performed in the past in other metrics, you can view this free graph of past earnings, revenue and cash flow.

So How Is Polwax's ROCE Trending?

We are a bit worried about the trend of returns on capital at Polwax. To be more specific, the ROCE was 33% five years ago, but since then it has dropped noticeably. Meanwhile, capital employed in the business has stayed roughly the flat over the period. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. If these trends continue, we wouldn't expect Polwax to turn into a multi-bagger.

On a side note, Polwax's current liabilities are still rather high at 53% of total assets. This effectively means that suppliers (or short-term creditors) are funding a large portion of the business, so just be aware that this can introduce some elements of risk. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

Our Take On Polwax's ROCE

In summary, it's unfortunate that Polwax is generating lower returns from the same amount of capital. Long term shareholders who've owned the stock over the last five years have experienced a 60% depreciation in their investment, so it appears the market might not like these trends either. Unless there is a shift to a more positive trajectory in these metrics, we would look elsewhere.

If you'd like to know more about Polwax, we've spotted 3 warning signs, and 1 of them is a bit concerning.

While Polwax may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:PWX

Polwax

Produces and distributes refined and renewable paraffin, waxes, and specialty industrial paraffin compositions.

Flawless balance sheet and good value.