Advertisement

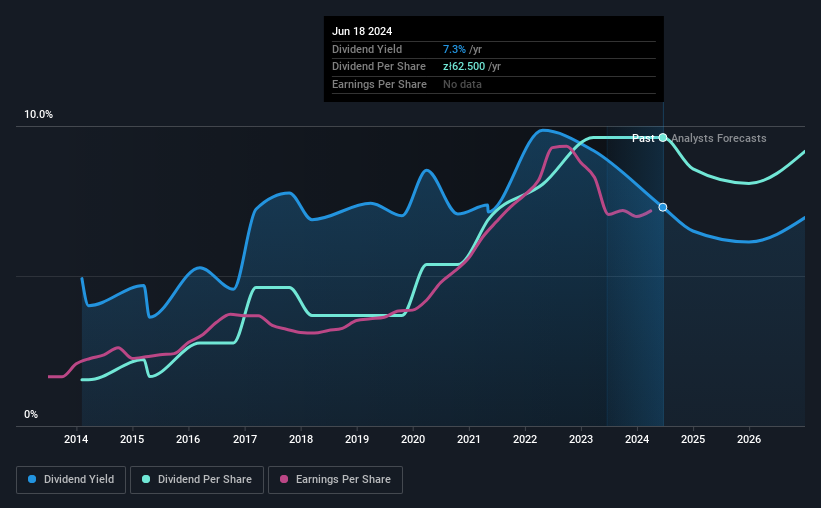

Grupa Kety S.A. (WSE:KTY) is reducing its dividend to PLN55.41 on the 6th of Novemberwhich is 11% less than last year's comparable payment of PLN62.50. However, the dividend yield of 7.3% is still a decent boost to shareholder returns.

See our latest analysis for Grupa Kety

Grupa Kety's Dividend Is Well Covered By Earnings

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Based on the last payment, the dividend made up 82% of cash flows, but a higher proportion of net income. While the cash payout ratio isn't necessarily a cause for concern, the company is probably focusing more on returning cash to shareholders than growing the business.

Over the next year, EPS is forecast to expand by 30.1%. Assuming the dividend continues along recent trends, our estimates say the payout ratio could reach 88% - on the higher side, but we wouldn't necessarily say this is unsustainable.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The annual payment during the last 10 years was PLN10.00 in 2014, and the most recent fiscal year payment was PLN62.50. This means that it has been growing its distributions at 20% per annum over that time. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

Dividend Growth Could Be Constrained

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. It's encouraging to see that Grupa Kety has been growing its earnings per share at 15% a year over the past five years. Although per-share earnings are growing at a credible rate, the massive payout ratio may limit growth in the company's future dividend payments.

The Dividend Could Prove To Be Unreliable

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. Strong earnings growth means Grupa Kety has the potential to be a good dividend stock in the future, despite the current payments being at elevated levels. Overall, we don't think this company has the makings of a good income stock.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. For example, we've picked out 1 warning sign for Grupa Kety that investors should know about before committing capital to this stock. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About WSE:KTY

Grupa Kety

Through its subsidiaries, manufactures and sells aluminum profiles and components in Poland and internationally.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor