- Poland

- /

- Metals and Mining

- /

- WSE:KGH

Optimistic Investors Push KGHM Polska Miedz S.A. (WSE:KGH) Shares Up 28% But Growth Is Lacking

The KGHM Polska Miedz S.A. (WSE:KGH) share price has done very well over the last month, posting an excellent gain of 28%. Taking a wider view, although not as strong as the last month, the full year gain of 17% is also fairly reasonable.

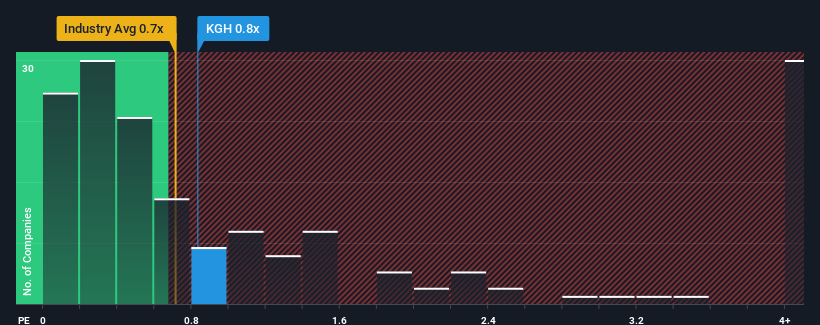

Even after such a large jump in price, there still wouldn't be many who think KGHM Polska Miedz's price-to-sales (or "P/S") ratio of 0.8x is worth a mention when the median P/S in Poland's Metals and Mining industry is similar at about 0.4x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

See our latest analysis for KGHM Polska Miedz

How Has KGHM Polska Miedz Performed Recently?

Recent times have been pleasing for KGHM Polska Miedz as its revenue has risen in spite of the industry's average revenue going into reverse. Perhaps the market is expecting its current strong performance to taper off in accordance to the rest of the industry, which has kept the P/S contained. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on KGHM Polska Miedz.Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, KGHM Polska Miedz would need to produce growth that's similar to the industry.

Retrospectively, the last year delivered virtually the same number to the company's top line as the year before. Still, the latest three year period has seen an excellent 51% overall rise in revenue, in spite of its uninspiring short-term performance. Therefore, it's fair to say the revenue growth recently has been great for the company, but investors will want to ask why it has slowed to such an extent.

Turning to the outlook, the next three years should bring diminished returns, with revenue decreasing 0.3% per annum as estimated by the ten analysts watching the company. Meanwhile, the broader industry is forecast to expand by 211% each year, which paints a poor picture.

With this information, we find it concerning that KGHM Polska Miedz is trading at a fairly similar P/S compared to the industry. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as these declining revenues are likely to weigh on the share price eventually.

What Does KGHM Polska Miedz's P/S Mean For Investors?

KGHM Polska Miedz appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our check of KGHM Polska Miedz's analyst forecasts revealed that its outlook for shrinking revenue isn't bringing down its P/S as much as we would have predicted. When we see a gloomy outlook like this, our immediate thoughts are that the share price is at risk of declining, negatively impacting P/S. If the poor revenue outlook tells us one thing, it's that these current price levels could be unsustainable.

Plus, you should also learn about these 2 warning signs we've spotted with KGHM Polska Miedz.

If these risks are making you reconsider your opinion on KGHM Polska Miedz, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if KGHM Polska Miedz might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:KGH

KGHM Polska Miedz

Engages in the production and sale of copper, precious metals, and non-ferrous metals in Poland and internationally.

Flawless balance sheet with moderate growth potential.