- Poland

- /

- Medical Equipment

- /

- WSE:MRC

Improved Revenues Required Before Mercator Medical S.A. (WSE:MRC) Stock's 31% Jump Looks Justified

Mercator Medical S.A. (WSE:MRC) shareholders would be excited to see that the share price has had a great month, posting a 31% gain and recovering from prior weakness. The last 30 days bring the annual gain to a very sharp 40%.

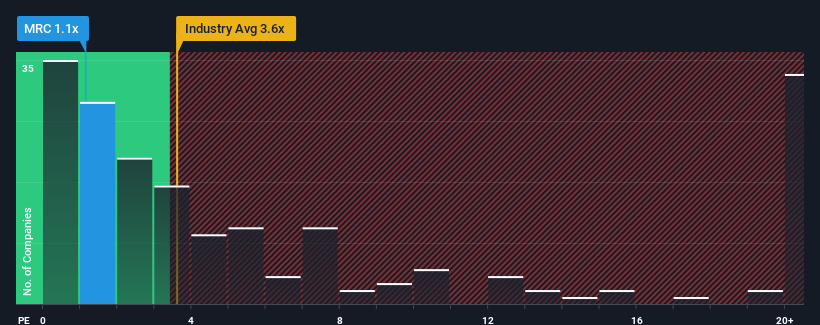

In spite of the firm bounce in price, Mercator Medical may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 1.1x, since almost half of all companies in the Medical Equipment industry in Poland have P/S ratios greater than 14.8x and even P/S higher than 460x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

Check out our latest analysis for Mercator Medical

What Does Mercator Medical's P/S Mean For Shareholders?

As an illustration, revenue has deteriorated at Mercator Medical over the last year, which is not ideal at all. Perhaps the market believes the recent revenue performance isn't good enough to keep up the industry, causing the P/S ratio to suffer. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Mercator Medical's earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For Mercator Medical?

Mercator Medical's P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 6.0%. As a result, revenue from three years ago have also fallen 78% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

In contrast to the company, the rest of the industry is expected to grow by 8.7% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

In light of this, it's understandable that Mercator Medical's P/S would sit below the majority of other companies. However, we think shrinking revenues are unlikely to lead to a stable P/S over the longer term, which could set up shareholders for future disappointment. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Final Word

Shares in Mercator Medical have risen appreciably however, its P/S is still subdued. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

It's no surprise that Mercator Medical maintains its low P/S off the back of its sliding revenue over the medium-term. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. If recent medium-term revenue trends continue, it's hard to see the share price moving strongly in either direction in the near future under these circumstances.

We don't want to rain on the parade too much, but we did also find 3 warning signs for Mercator Medical (1 is potentially serious!) that you need to be mindful of.

If these risks are making you reconsider your opinion on Mercator Medical, explore our interactive list of high quality stocks to get an idea of what else is out there.

If you're looking to trade Mercator Medical, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:MRC

Mercator Medical

Manufactures and distributes disposable medical gloves, dressings, and non-woven fabric products in Poland, the Czech Republic, Ukraine, France, Hungary, Italy, Romania, Germany, rest of Europe, and Thailand.

Excellent balance sheet and slightly overvalued.