Advertisement

- Poland

- /

- Consumer Durables

- /

- WSE:1AT

Most Shareholders Will Probably Agree With Atal S.A.'s (WSE:1AT) CEO Compensation

Key Insights

- Atal to hold its Annual General Meeting on 17th of June

- Total pay for CEO Zbigniew Juroszek includes zł364.0k salary

- The overall pay is 90% below the industry average

- Over the past three years, Atal's EPS fell by 21% and over the past three years, the total shareholder return was 139%

Shareholders may be wondering what CEO Zbigniew Juroszek plans to do to improve the less than great performance at Atal S.A. (WSE:1AT) recently. At the next AGM coming up on 17th of June, they can influence managerial decision making through voting on resolutions, including executive remuneration. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. In our opinion, CEO compensation does not look excessive and we discuss why.

Check out our latest analysis for Atal

How Does Total Compensation For Zbigniew Juroszek Compare With Other Companies In The Industry?

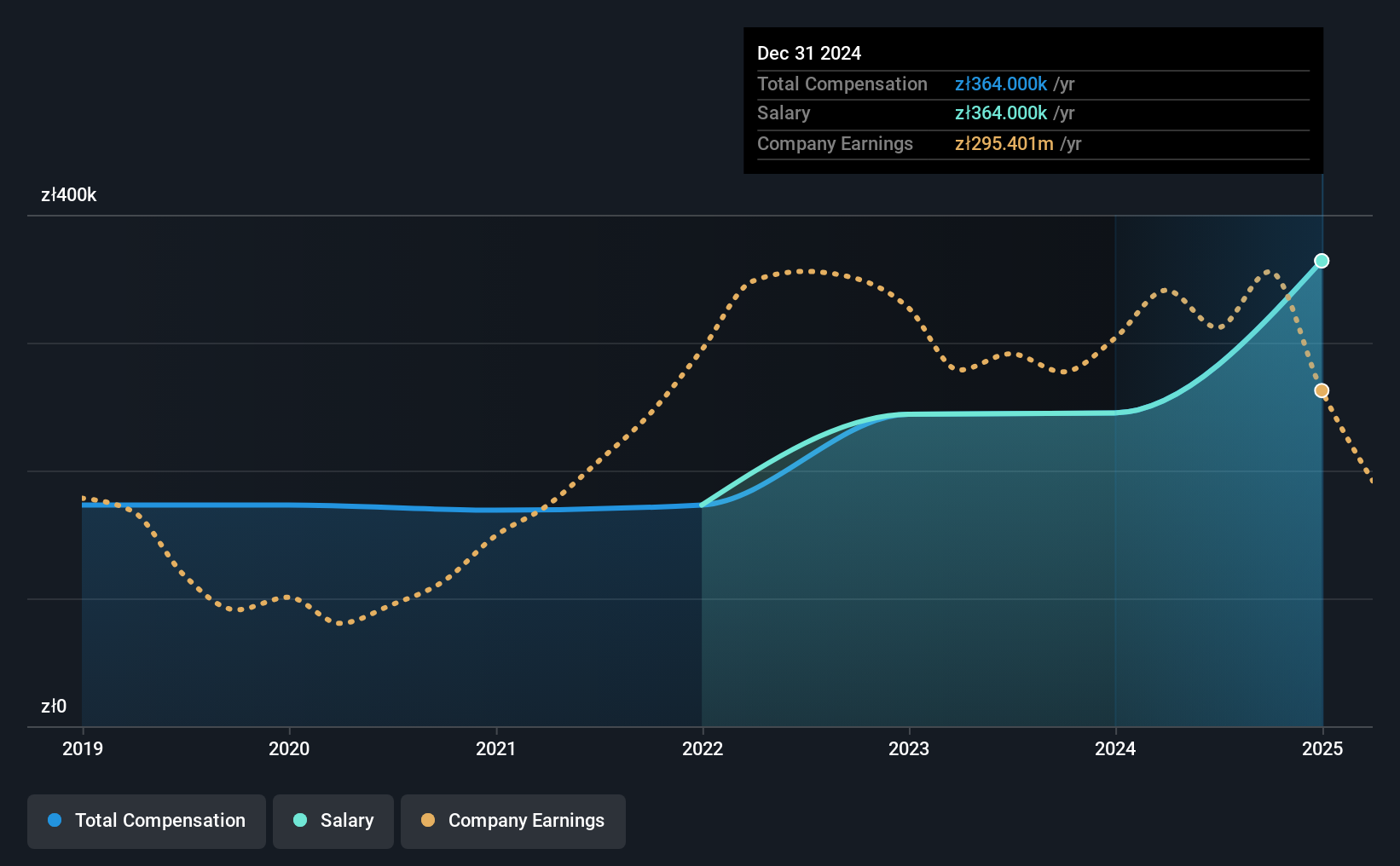

At the time of writing, our data shows that Atal S.A. has a market capitalization of zł2.9b, and reported total annual CEO compensation of zł364k for the year to December 2024. We note that's an increase of 49% above last year. Notably, the salary of zł364k is the entirety of the CEO compensation.

For comparison, other companies in the Polish Consumer Durables industry with market capitalizations ranging between zł1.5b and zł6.0b had a median total CEO compensation of zł3.6m. That is to say, Zbigniew Juroszek is paid under the industry median. Furthermore, Zbigniew Juroszek directly owns zł2.2b worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | zł364k | zł245k | 100% |

| Other | - | - | - |

| Total Compensation | zł364k | zł245k | 100% |

On an industry level, roughly 92% of total compensation represents salary and 8% is other remuneration. At the company level, Atal pays Zbigniew Juroszek solely through a salary, preferring to go down a conventional route. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Atal S.A.'s Growth Numbers

Atal S.A. has reduced its earnings per share by 21% a year over the last three years. In the last year, its revenue is down 28%.

The decline in EPS is a bit concerning. And the impression is worse when you consider revenue is down year-on-year. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Atal S.A. Been A Good Investment?

Boasting a total shareholder return of 139% over three years, Atal S.A. has done well by shareholders. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

Atal rewards its CEO solely through a salary, ignoring non-salary benefits completely. Although shareholders would be quite happy with the returns they have earned on their initial investment, earnings have failed to grow and this could mean these strong returns may not continue. Shareholders might want to question the board about these concerns, and revisit their investment thesis for the company.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 3 warning signs for Atal that you should be aware of before investing.

Switching gears from Atal, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:1AT

Atal

Engages in the construction and sale of residential real estate and the rental of commercial real estate in Poland.

Very undervalued with high growth potential.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

9 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9238.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.6% undervalued

946 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.2% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative