Advertisement

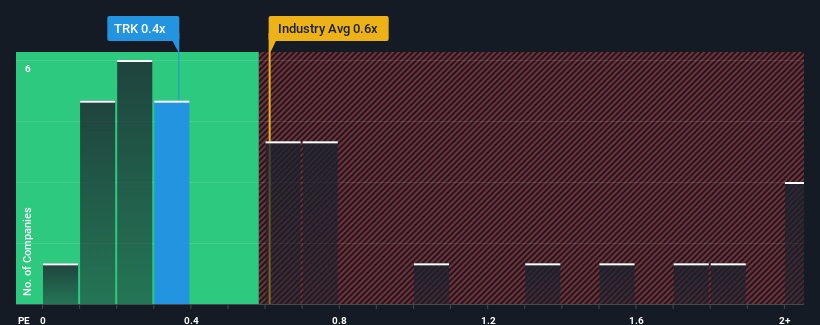

It's not a stretch to say that Trakcja S.A.'s (WSE:TRK) price-to-sales (or "P/S") ratio of 0.4x right now seems quite "middle-of-the-road" for companies in the Construction industry in Poland, where the median P/S ratio is around 0.6x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Trakcja

What Does Trakcja's Recent Performance Look Like?

With revenue growth that's exceedingly strong of late, Trakcja has been doing very well. The P/S is probably moderate because investors think this strong revenue growth might not be enough to outperform the broader industry in the near future. Those who are bullish on Trakcja will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Trakcja's earnings, revenue and cash flow.Do Revenue Forecasts Match The P/S Ratio?

Trakcja's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, we see that the company grew revenue by an impressive 39% last year. The strong recent performance means it was also able to grow revenue by 60% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

When compared to the industry's one-year growth forecast of 11%, the most recent medium-term revenue trajectory is noticeably more alluring

In light of this, it's curious that Trakcja's P/S sits in line with the majority of other companies. It may be that most investors are not convinced the company can maintain its recent growth rates.

The Key Takeaway

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that Trakcja currently trades on a lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. It'd be fair to assume that potential risks the company faces could be the contributing factor to the lower than expected P/S. It appears some are indeed anticipating revenue instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Trakcja that you should be aware of.

If you're unsure about the strength of Trakcja's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Trakcja might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:TRK

Trakcja

Operates in the infrastructure and energy construction sector in Poland and internationally.

Excellent balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.9% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.9% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|64.1% undervalued

ME

Community Contributor