PGF Polska Grupa Fotowoltaiczna (WSE:PGV) Has A Somewhat Strained Balance Sheet

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies PGF Polska Grupa Fotowoltaiczna SA (WSE:PGV) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for PGF Polska Grupa Fotowoltaiczna

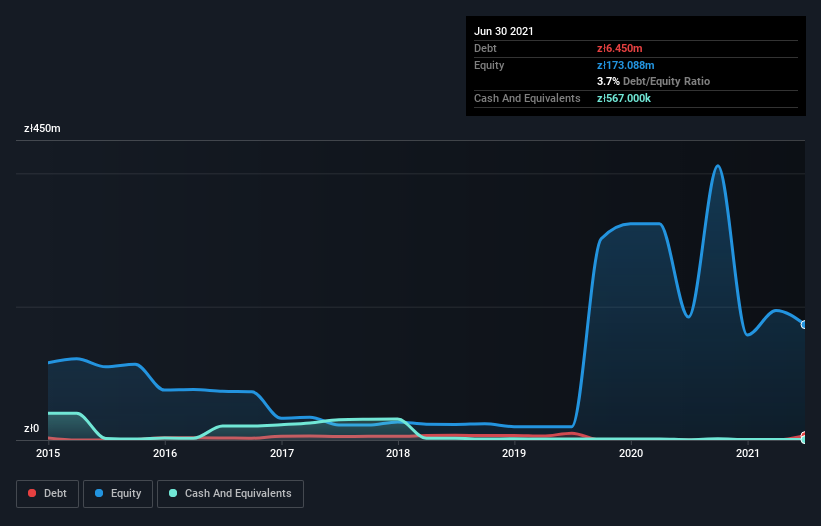

How Much Debt Does PGF Polska Grupa Fotowoltaiczna Carry?

As you can see below, at the end of June 2021, PGF Polska Grupa Fotowoltaiczna had zł6.45m of debt, up from none a year ago. Click the image for more detail. On the flip side, it has zł567.0k in cash leading to net debt of about zł5.88m.

How Strong Is PGF Polska Grupa Fotowoltaiczna's Balance Sheet?

The latest balance sheet data shows that PGF Polska Grupa Fotowoltaiczna had liabilities of zł19.2m due within a year, and liabilities of zł34.5m falling due after that. On the other hand, it had cash of zł567.0k and zł29.6m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by zł23.6m.

Of course, PGF Polska Grupa Fotowoltaiczna has a market capitalization of zł145.5m, so these liabilities are probably manageable. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

PGF Polska Grupa Fotowoltaiczna shareholders face the double whammy of a high net debt to EBITDA ratio (69.6), and fairly weak interest coverage, since EBIT is just 2.1 times the interest expense. This means we'd consider it to have a heavy debt load. However, the silver lining was that PGF Polska Grupa Fotowoltaiczna achieved a positive EBIT of zł83k in the last twelve months, an improvement on the prior year's loss. There's no doubt that we learn most about debt from the balance sheet. But it is PGF Polska Grupa Fotowoltaiczna's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of the earnings before interest and tax (EBIT) is backed by free cash flow. During the last year, PGF Polska Grupa Fotowoltaiczna burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

On the face of it, PGF Polska Grupa Fotowoltaiczna's net debt to EBITDA left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability to handle its total liabilities isn't such a worry. Looking at the bigger picture, it seems clear to us that PGF Polska Grupa Fotowoltaiczna's use of debt is creating risks for the company. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 4 warning signs with PGF Polska Grupa Fotowoltaiczna (at least 1 which shouldn't be ignored) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About WSE:PGV

Flawless balance sheet low.