- Poland

- /

- Construction

- /

- WSE:MSZ

These 4 Measures Indicate That Mostostal Zabrze (WSE:MSZ) Is Using Debt Reasonably Well

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Mostostal Zabrze S.A. (WSE:MSZ) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Mostostal Zabrze

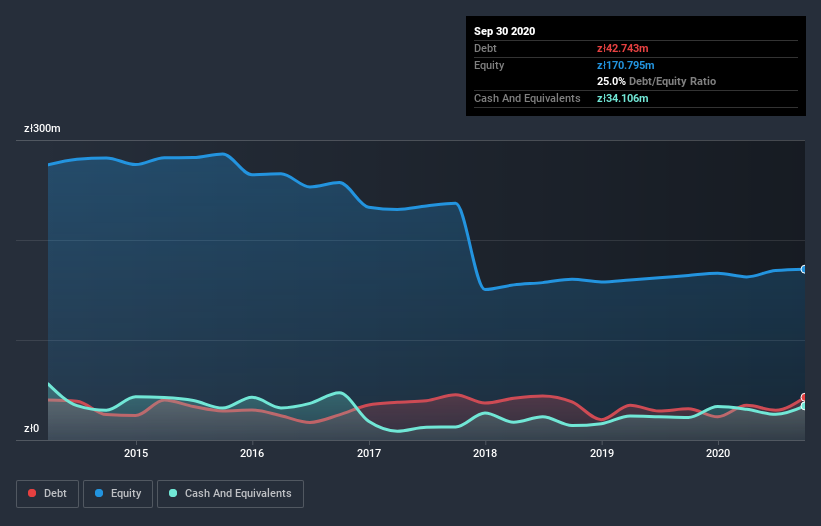

How Much Debt Does Mostostal Zabrze Carry?

You can click the graphic below for the historical numbers, but it shows that as of September 2020 Mostostal Zabrze had zł42.7m of debt, an increase on zł31.2m, over one year. However, it also had zł34.1m in cash, and so its net debt is zł8.64m.

A Look At Mostostal Zabrze's Liabilities

According to the last reported balance sheet, Mostostal Zabrze had liabilities of zł231.8m due within 12 months, and liabilities of zł56.3m due beyond 12 months. Offsetting these obligations, it had cash of zł34.1m as well as receivables valued at zł215.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by zł39.0m.

While this might seem like a lot, it is not so bad since Mostostal Zabrze has a market capitalization of zł102.9m, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Mostostal Zabrze's net debt is only 0.27 times its EBITDA. And its EBIT easily covers its interest expense, being 12.7 times the size. So you could argue it is no more threatened by its debt than an elephant is by a mouse. The good news is that Mostostal Zabrze has increased its EBIT by 7.9% over twelve months, which should ease any concerns about debt repayment. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Mostostal Zabrze will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last two years, Mostostal Zabrze recorded negative free cash flow, in total. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

Mostostal Zabrze's interest cover was a real positive on this analysis, as was its net debt to EBITDA. In contrast, our confidence was undermined by its apparent struggle to convert EBIT to free cash flow. When we consider all the factors mentioned above, we do feel a bit cautious about Mostostal Zabrze's use of debt. While debt does have its upside in higher potential returns, we think shareholders should definitely consider how debt levels might make the stock more risky. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 3 warning signs for Mostostal Zabrze that you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you decide to trade Mostostal Zabrze, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About WSE:MSZ

Mostostal Zabrze

Engages in the design, production, construction, and assembly activities.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives