Advertisement

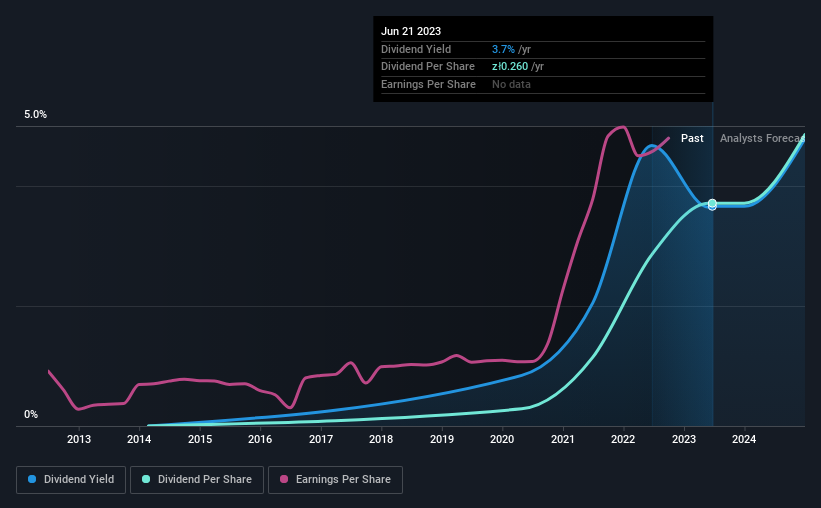

Mirbud S.A.'s (WSE:MRB) dividend will be increasing from last year's payment of the same period to PLN0.26 on 21st of July. This takes the annual payment to 3.7% of the current stock price, which unfortunately is below what the industry is paying.

Check out our latest analysis for Mirbud

Mirbud's Earnings Easily Cover The Distributions

It would be nice for the yield to be higher, but we should also check if higher levels of dividend payment would be sustainable. Based on the last payment, Mirbud was earning enough to cover the dividend, but free cash flows weren't positive. With the company not bringing in any cash, paying out to shareholders is bound to become difficult at some point.

Over the next year, EPS could expand by 46.3% if recent trends continue. If the dividend continues on this path, the payout ratio could be 14% by next year, which we think can be pretty sustainable going forward.

Mirbud Is Still Building Its Track Record

The company has maintained a consistent dividend for a few years now, but we would like to see a longer track record before relying on it. The dividend has gone from an annual total of PLN0.02 in 2020 to the most recent total annual payment of PLN0.26. This means that it has been growing its distributions at 135% per annum over that time. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Mirbud has impressed us by growing EPS at 46% per year over the past five years. Earnings per share is growing at a solid clip, and the payout ratio is low which we think is an ideal combination in a dividend stock as the company can quite easily raise the dividend in the future.

Our Thoughts On Mirbud's Dividend

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. While Mirbud is earning enough to cover the payments, the cash flows are lacking. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 3 warning signs for Mirbud (of which 1 is potentially serious!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WSE:MRB

Mirbud

Operates as a general contractor in the construction industry in Poland.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|34.2% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|19.8% undervalued

MI

Community Contributor