Advertisement

- New Zealand

- /

- Electric Utilities

- /

- NZSE:CEN

Why It Might Not Make Sense To Buy Contact Energy Limited (NZSE:CEN) For Its Upcoming Dividend

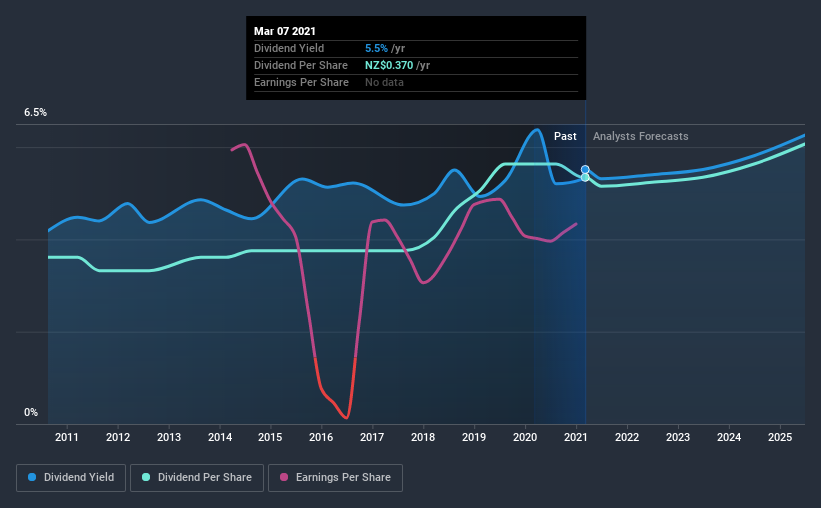

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Contact Energy Limited (NZSE:CEN) is about to go ex-dividend in just 4 days. You can purchase shares before the 12th of March in order to receive the dividend, which the company will pay on the 30th of March.

Contact Energy's upcoming dividend is NZ$0.16 a share, following on from the last 12 months, when the company distributed a total of NZ$0.37 per share to shareholders. Based on the last year's worth of payments, Contact Energy has a trailing yield of 5.5% on the current stock price of NZ$6.71. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

View our latest analysis for Contact Energy

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Contact Energy paid out 185% of profit in the past year, which we think is typically not sustainable unless there are mitigating characteristics such as unusually strong cash flow or a large cash balance. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. It paid out 96% of its free cash flow in the form of dividends last year, which is outside the comfort zone for most businesses. Cash flows are usually much more volatile than earnings, so this could be a temporary effect - but we'd generally want look more closely here.

Cash is slightly more important than profit from a dividend perspective, but given Contact Energy's payouts were not well covered by either earnings or cash flow, we would be concerned about the sustainability of this dividend.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Stocks with flat earnings can still be attractive dividend payers, but it is important to be more conservative with your approach and demand a greater margin for safety when it comes to dividend sustainability. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. It's not encouraging to see that Contact Energy's earnings are effectively flat over the past five years. We'd take that over an earnings decline any day, but in the long run, the best dividend stocks all grow their earnings per share. Earnings are not growing much and Contact Energy paid out a lot more than it earned in profit last year. This makes the dividend look potentially unsustainable in the long run.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Contact Energy has delivered 4.0% dividend growth per year on average over the past 10 years.

Final Takeaway

From a dividend perspective, should investors buy or avoid Contact Energy? Contact Energy is paying out an uncomfortably high percentage of both earnings and cash flow as dividends, at the same time as its earnings per share are struggling to grow. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

So if you're still interested in Contact Energy despite it's poor dividend qualities, you should be well informed on some of the risks facing this stock. For example, we've found 4 warning signs for Contact Energy (1 shouldn't be ignored!) that deserve your attention before investing in the shares.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade Contact Energy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NZSE:CEN

Contact Energy

Generates and sells electricity and natural gas in New Zealand.

Solid track record with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor