- New Zealand

- /

- Insurance

- /

- NZSE:TWR

Tower Limited's (NZSE:TWR) On An Uptrend But Financial Prospects Look Pretty Weak: Is The Stock Overpriced?

Tower (NZSE:TWR) has had a great run on the share market with its stock up by a significant 55% over the last three months. However, in this article, we decided to focus on its weak fundamentals, as long-term financial performance of a business is what ultimately dictates market outcomes. In this article, we decided to focus on Tower's ROE.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Tower

How Do You Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Tower is:

10% = NZ$35m ÷ NZ$334m (Based on the trailing twelve months to March 2024).

The 'return' is the amount earned after tax over the last twelve months. That means that for every NZ$1 worth of shareholders' equity, the company generated NZ$0.10 in profit.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. We now need to evaluate how much profit the company reinvests or "retains" for future growth which then gives us an idea about the growth potential of the company. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

A Side By Side comparison of Tower's Earnings Growth And 10% ROE

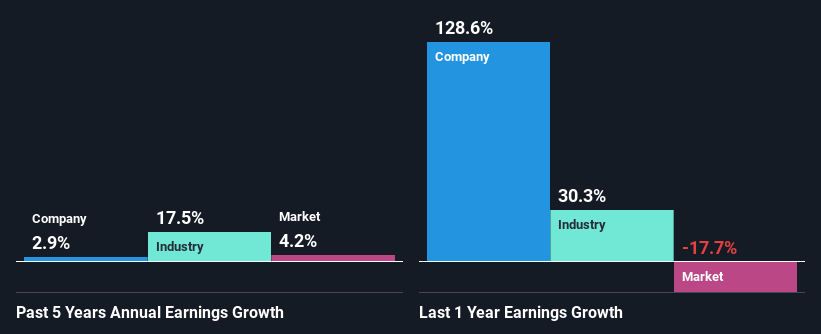

On the face of it, Tower's ROE is not much to talk about. Yet, a closer study shows that the company's ROE is similar to the industry average of 11%. Having said that, Tower has shown a meagre net income growth of 2.9% over the past five years. Remember, the company's ROE is not particularly great to begin with. Hence, this does provide some context to low earnings growth seen by the company.

We then compared Tower's net income growth with the industry and found that the company's growth figure is lower than the average industry growth rate of 17% in the same 5-year period, which is a bit concerning.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. This then helps them determine if the stock is placed for a bright or bleak future. Is Tower fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is Tower Efficiently Re-investing Its Profits?

Tower's very high three-year median payout ratio of 125% suggests that the company is paying its shareholders more than what it is earning and it definitely contributes to the low earnings growth seen by the company. This is quite a risky position to be in.

Additionally, Tower has paid dividends over a period of at least ten years, which means that the company's management is determined to pay dividends even if it means little to no earnings growth. Our latest analyst data shows that the future payout ratio of the company is expected to drop to 69% over the next three years. Accordingly, the expected drop in the payout ratio explains the expected increase in the company's ROE to 19%, over the same period.

Summary

On the whole, Tower's performance is quite a big let-down. Particularly, its ROE is a huge disappointment, not to mention its lack of proper reinvestment into the business. As a result its earnings growth has also been quite disappointing. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

Valuation is complex, but we're here to simplify it.

Discover if Tower might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NZSE:TWR

Tower

Provides general insurance products in New Zealand and the Pacific Islands.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives