Thin Film Electronics ASA (OB:THIN) continues its loss-making streak, announcing negative earnings for its latest financial year ending. A crucial question to bear in mind when you’re an investor of an unprofitable business, is whether the company will have to raise more capital in the near future. Cash is crucial to run a business, and if a company burns through its reserves fast, it will need to raise further funds. This may not always be on good terms, which could hurt current shareholders if the new deal lowers the value of their shares. Thin Film Electronics may need to come to market again, but the question is, when? Below, I’ve analysed the most recent financial data to help answer this question.

View our latest analysis for Thin Film Electronics

What is cash burn?

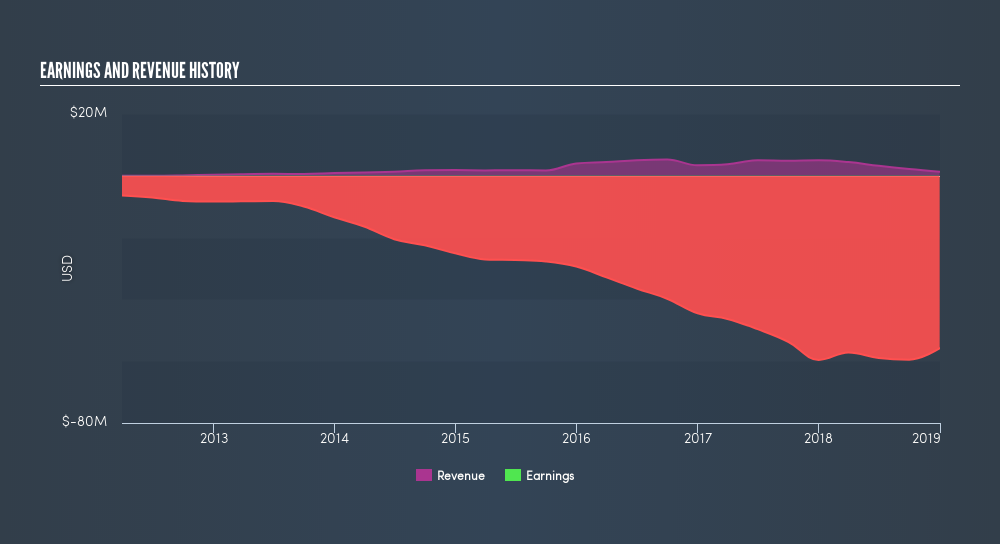

Currently, Thin Film Electronics has US$33m in cash holdings and producing negative free cash flow of -US$65.0m. The riskiest factor facing investors of Thin Film Electronics is the potential for the company to run out of cash without the ability to raise more money. Furthermore, it is not uncommon to find loss-makers in an industry such as tech. These companies face the trade-off between running the risk of depleting its cash reserves too fast, or falling behind competition on innovation and gaining market share by investing too slowly.

When will Thin Film Electronics need to raise more cash?

One way to measure the cost to Thin Film Electronics of keeping the business running, is by using free cash flow (which I define as cash flow from operations minus fixed capital investment).

Free cash outflows declined by 27% over the past year, which could be an indication of Thin Film Electronics putting the brakes on ramping up high growth. Given the level of cash left in the bank, if Thin Film Electronics maintained its cash burn rate of -US$65.0m, it could still run out of cash within the next few of months. Even though this is analysis is fairly basic, and Thin Film Electronics still can cut its overhead further, or open a new line of credit instead of issuing new shares, this analysis still helps us understand how sustainable the Thin Film Electronics operation is, and when things may have to change.

Next Steps:

Loss-making companies are a risky play, even those that are reducing their cash burn over time. Though, this shouldn’t discourage you from considering entering the stock in the future. The outcome of my analysis suggests that even if the company maintains this rate of cash burn growth, it will run out of cash within the year. An opportunity may exist for you to enter into the stock at an attractive price, should Thin Film Electronics be required to raise new funds to continue operating. I admit this is a fairly basic analysis for THIN's financial health. Other important fundamentals need to be considered as well. I recommend you continue to research Thin Film Electronics to get a more holistic view of the company by looking at:- Future Outlook: What are well-informed industry analysts predicting for THIN’s future growth? Take a look at our free research report of analyst consensus for THIN’s outlook.

- Valuation: What is THIN worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether THIN is currently mispriced by the market.

- Other High-Performing Stocks: If you believe you should cushion your portfolio with something less risky, scroll through our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 31 December 2018. This may not be consistent with full year annual report figures. Operating expenses include only SG&A and one-year R&D.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About OB:ENSU

Ensurge Micropower

Provides energy storage solutions for wearable devices, connected sensors, and other applications in Norway.

Moderate with imperfect balance sheet.