- Norway

- /

- Communications

- /

- OB:NAPA

Need To Know: This Analyst Just Made A Substantial Cut To Their Napatech A/S (OB:NAPA) Estimates

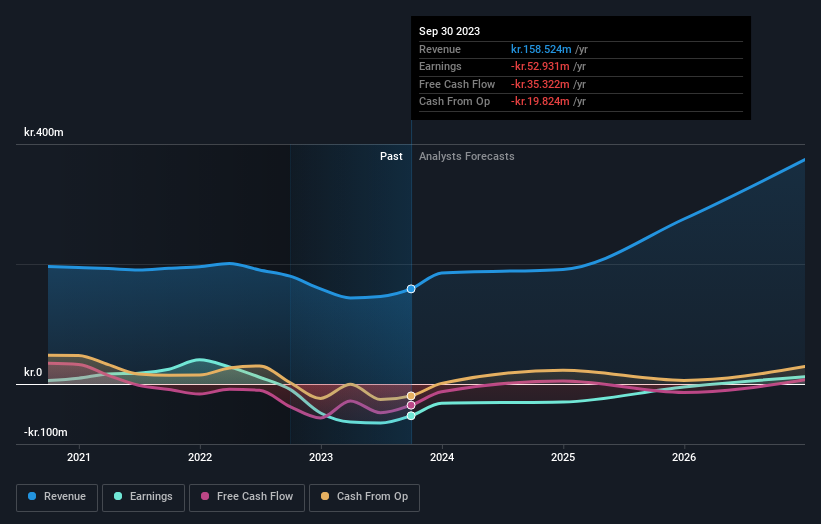

One thing we could say about the covering analyst on Napatech A/S (OB:NAPA) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business.

Following the downgrade, the latest consensus from Napatech's solo analyst is for revenues of kr.191m in 2024, which would reflect a sizeable 20% improvement in sales compared to the last 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 42% to kr.0.34. However, before this estimates update, the consensus had been expecting revenues of kr.231m and kr.0.19 per share in losses. So there's been quite a change-up of views after the recent consensus updates, with the analyst making a serious cut to their revenue forecasts while also expecting losses per share to increase.

See our latest analysis for Napatech

The consensus price target lifted 36% to kr.11.77, clearly signalling that the weaker revenue and EPS outlook are not expected to weigh on the stock over the longer term.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that Napatech's rate of growth is expected to accelerate meaningfully, with the forecast 16% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 4.7% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 2.3% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Napatech is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that the analyst increased their loss per share estimates for next year. Unfortunately, the analyst also downgraded their revenue estimates, although our data indicates revenues are expected to perform better than the wider market. The increasing price target is not intuitively what we would expect to see, given these downgrades, and we'd suggest shareholders revisit their investment thesis before making a decision.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have analyst estimates for Napatech going out as far as 2026, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Napatech might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:NAPA

Napatech

Provides programmable smart network interface cards and infrastructure processing units for cloud, enterprise, and telecom datacenter networks in the Americas and internationally.

Flawless balance sheet with very low risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion