- Norway

- /

- Specialty Stores

- /

- OB:KOMPL

Earnings Release: Here's Why Analysts Cut Their Komplett ASA (OB:KOMPL) Price Target To kr11.50

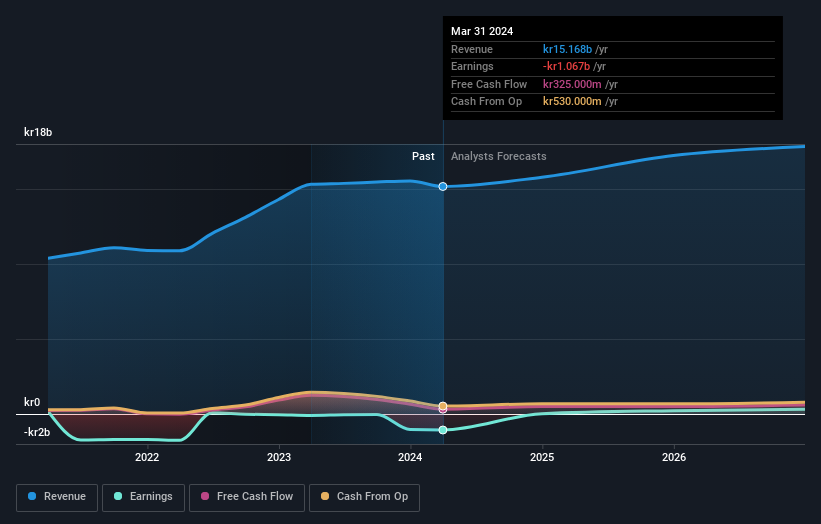

Komplett ASA (OB:KOMPL) just released its latest first-quarter report and things are not looking great. It was a pretty negative result overall, with revenues of kr3.2b missing analyst predictions by 6.1%. Worse, the business reported a statutory loss of kr0.41 per share, much larger than the analysts had forecast prior to the result. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

See our latest analysis for Komplett

Taking into account the latest results, the most recent consensus for Komplett from three analysts is for revenues of kr15.8b in 2024. If met, it would imply a modest 4.1% increase on its revenue over the past 12 months. Komplett is also expected to turn profitable, with statutory earnings of kr0.48 per share. In the lead-up to this report, the analysts had been modelling revenues of kr16.2b and earnings per share (EPS) of kr0.58 in 2024. The analysts seem less optimistic after the recent results, reducing their revenue forecasts and making a substantial drop in earnings per share numbers.

The consensus price target fell 12% to kr11.50, with the weaker earnings outlook clearly leading valuation estimates. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Komplett, with the most bullish analyst valuing it at kr13.00 and the most bearish at kr10.00 per share. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Komplett is an easy business to forecast or the the analysts are all using similar assumptions.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Komplett's revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 5.5% growth on an annualised basis. This is compared to a historical growth rate of 16% over the past three years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 6.0% annually. So it's pretty clear that, while Komplett's revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Komplett. They also downgraded their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Komplett's future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on Komplett. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Komplett analysts - going out to 2026, and you can see them free on our platform here.

You can also see whether Komplett is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

Valuation is complex, but we're here to simplify it.

Discover if Komplett might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:KOMPL

Komplett

Operates as an online retailer of electronics products in Norway, Sweden, and Denmark.

Flawless balance sheet and undervalued.