Advertisement

Europris ASA's (OB:EPR) CEO Compensation Is Looking A Bit Stretched At The Moment

Key Insights

- Europris' Annual General Meeting to take place on 30th of April

- Total pay for CEO Espen Eldal includes kr4.18m salary

- The overall pay is 154% above the industry average

- Over the past three years, Europris' EPS grew by 5.1% and over the past three years, the total shareholder return was 65%

Performance at Europris ASA (OB:EPR) has been reasonably good and CEO Espen Eldal has done a decent job of steering the company in the right direction. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 30th of April. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

View our latest analysis for Europris

Comparing Europris ASA's CEO Compensation With The Industry

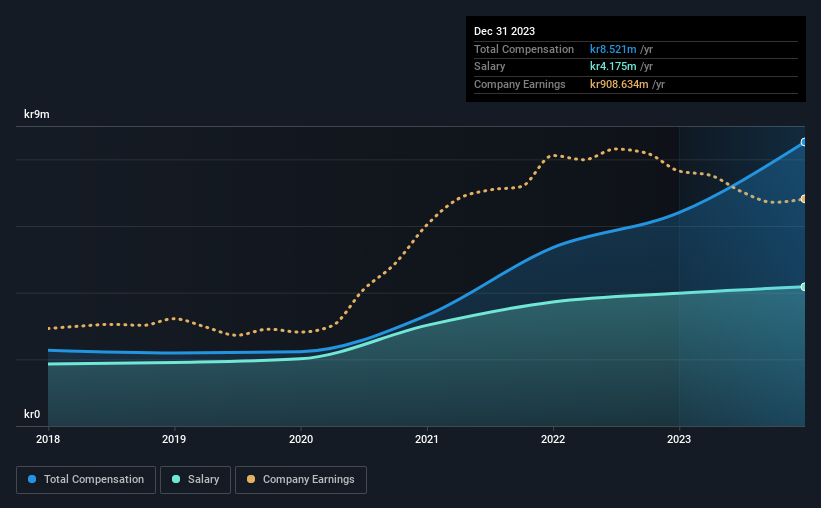

According to our data, Europris ASA has a market capitalization of kr13b, and paid its CEO total annual compensation worth kr8.5m over the year to December 2023. That's a notable increase of 33% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at kr4.2m.

In comparison with other companies in the Norway Multiline Retail industry with market capitalizations ranging from kr4.4b to kr17b, the reported median CEO total compensation was kr3.4m. Hence, we can conclude that Espen Eldal is remunerated higher than the industry median. Furthermore, Espen Eldal directly owns kr49m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | kr4.2m | kr4.0m | 49% |

| Other | kr4.3m | kr2.4m | 51% |

| Total Compensation | kr8.5m | kr6.4m | 100% |

On an industry level, roughly 49% of total compensation represents salary and 51% is other remuneration. There isn't a significant difference between Europris and the broader market, in terms of salary allocation in the overall compensation package. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

Europris ASA's Growth

Europris ASA has seen its earnings per share (EPS) increase by 5.1% a year over the past three years. In the last year, its revenue is up 5.0%.

We're not particularly impressed by the revenue growth, but we're happy with the modest EPS growth. So there are some positives here, but not enough to earn high praise. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Europris ASA Been A Good Investment?

We think that the total shareholder return of 65%, over three years, would leave most Europris ASA shareholders smiling. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 1 warning sign for Europris that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Europris might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:EPR

Established dividend payer with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

75 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8147.4% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

89 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

926 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative