Storebrand (OB:STB) has been catching the attention of investors lately, not because of headline-grabbing news or dramatic market shocks, but thanks to a string of gains that raise questions about the stock’s true worth. Its steady climb over the past months stands out in a market that has rewarded consistency, and the company’s most recent closing price is quietly nudging investors to re-examine their expectations. Sometimes, it is these quiet movers, rather than the uproar of breaking news, that end up offering the most interesting valuation puzzles.

Looking past the headlines, Storebrand has posted an impressive 39% return over the past year and more than doubled over three years. Momentum seems to be building, especially when you note a 13% gain over the past three months and a healthy year-to-date performance of 26%. While annual revenue has edged down recently, net income has still managed modest growth, painting a mixed picture of financial health.

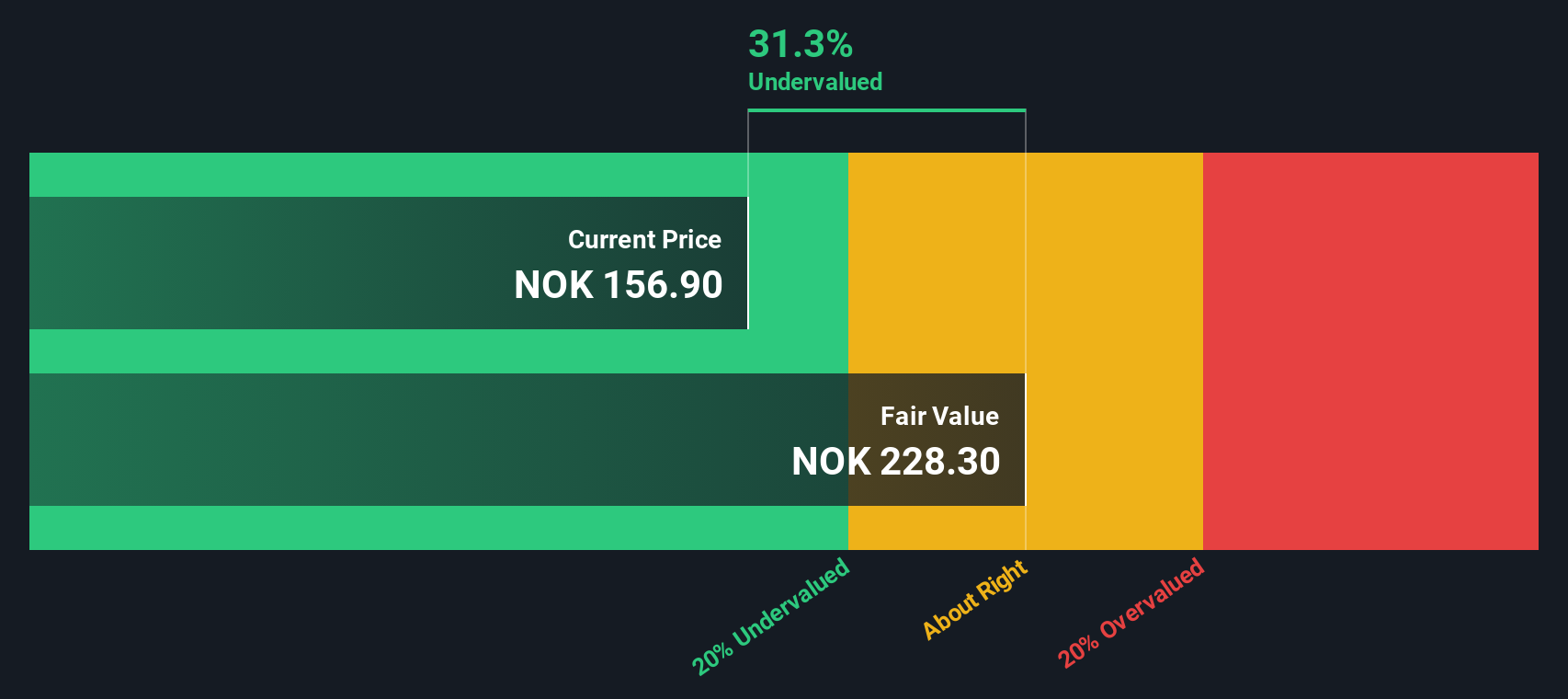

So, with a year of quiet but significant progress in the rearview mirror, is Storebrand now an undervalued opportunity in a steady market, or has all that growth already been priced in?

Advertisement

Most Popular Narrative: 174.6% Overvalued

The prevailing narrative values Storebrand as significantly overvalued, contending that its market price far exceeds assumptions for future profit and revenue.

Storebrand's strategic growth, sustainability leadership, and financial maneuvers strengthen its revenue potential, brand value, and shareholder returns. These efforts also boost future asset management growth. Catalysts About Storebrand: Provides insurance products and services in Norway, the United States, Japan, and Sweden.

Curious how such aggressive growth ambitions stack up against bold financial forecasts? The case hinges on rapidly shifting profit margins and ambitious assumptions for operating performance. Wondering how this turns into one of the market’s most stretched valuation calls? Take a closer look and discover which underlying projections fuel this contrarian price target calculation.

However, strong cost controls and successful acquisitions could boost revenue and earnings and challenge current assumptions of overvaluation in Storebrand's outlook.

Looking at Storebrand through the lens of our DCF model, the stock appears undervalued. This challenges the earlier view that it is overpriced. Could longer-term cash flows change the story?

If you see things differently or would rather shape the story for yourself, you can build your own narrative quickly and easily. Do it your way with Do it your way.

Don't let great opportunities pass you by. Go beyond Storebrand and get ahead of the curve with tailored investment ideas from market specialists and trendsetters using the Simply Wall Street Screener.

Capitalize on tomorrow’s breakthroughs by scanning for innovations in high-potential AI-driven firms with AI penny stocks.

Boost your passive income strategy by zeroing in on companies delivering stable payouts through dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.