With EPS Growth And More, Protector Forsikring (OB:PROT) Is Interesting

It's only natural that many investors, especially those who are new to the game, prefer to buy shares in 'sexy' stocks with a good story, even if those businesses lose money. And in their study titled Who Falls Prey to the Wolf of Wall Street?' Leuz et. al. found that it is 'quite common' for investors to lose money by buying into 'pump and dump' schemes.

So if you're like me, you might be more interested in profitable, growing companies, like Protector Forsikring (OB:PROT). While that doesn't make the shares worth buying at any price, you can't deny that successful capitalism requires profit, eventually. In comparison, loss making companies act like a sponge for capital - but unlike such a sponge they do not always produce something when squeezed.

Check out our latest analysis for Protector Forsikring

Protector Forsikring's Improving Profits

Over the last three years, Protector Forsikring has grown earnings per share (EPS) like young bamboo after rain; fast, and from a low base. So I don't think the percent growth rate is particularly meaningful. As a result, I'll zoom in on growth over the last year, instead. Like a firecracker arcing through the night sky, Protector Forsikring's EPS shot from kr5.88 to kr15.94, over the last year. Year on year growth of 171% is certainly a sight to behold.

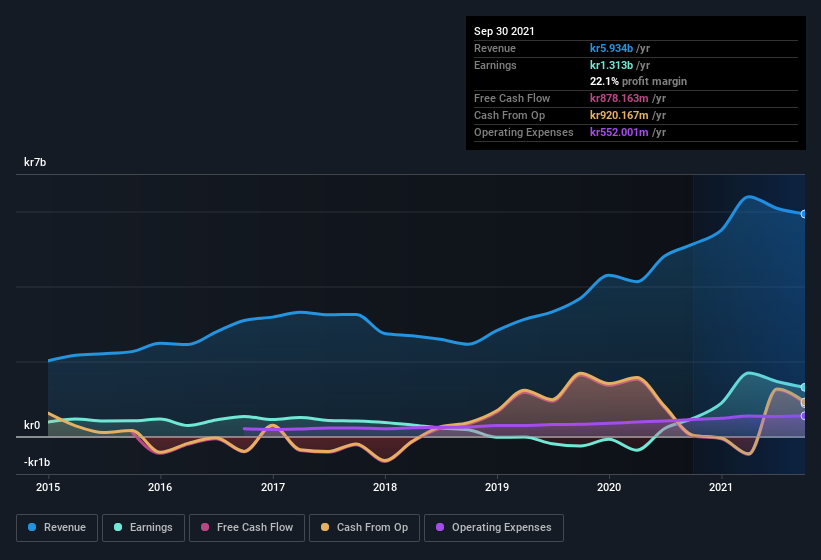

I like to see top-line growth as an indication that growth is sustainable, and I look for a high earnings before interest and taxation (EBIT) margin to point to a competitive moat (though some companies with low margins also have moats). Not all of Protector Forsikring's revenue this year is revenue from operations, so keep in mind the revenue and margin numbers I've used might not be the best representation of the underlying business. Protector Forsikring shareholders can take confidence from the fact that EBIT margins are up from 11% to 26%, and revenue is growing. That's great to see, on both counts.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

While it's always good to see growing profits, you should always remember that a weak balance sheet could come back to bite. So check Protector Forsikring's balance sheet strength, before getting too excited.

Are Protector Forsikring Insiders Aligned With All Shareholders?

Like the kids in the streets standing up for their beliefs, insider share purchases give me reason to believe in a brighter future. Because oftentimes, the purchase of stock is a sign that the buyer views it as undervalued. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

Although we did see some insider selling (worth -kr2.5m) this was overshadowed by a mountain of buying, totalling kr18m in just one year. This makes me even more interested in Protector Forsikring because it suggests that those who understand the company best, are optimistic. We also note that it was the Independent Deputy Chairman, Arve Ree, who made the biggest single acquisition, paying kr13m for shares at about kr91.10 each.

On top of the insider buying, it's good to see that Protector Forsikring insiders have a valuable investment in the business. With a whopping kr467m worth of shares as a group, insiders have plenty riding on the company's success. That's certainly enough to make me think that management will be very focussed on long term growth.

While insiders already own a significant amount of shares, and they have been buying more, the good news for ordinary shareholders does not stop there. The cherry on top is that the CEO, Henrik Hoye is paid comparatively modestly to CEOs at similar sized companies. I discovered that the median total compensation for the CEOs of companies like Protector Forsikring with market caps between kr3.5b and kr14b is about kr5.2m.

The Protector Forsikring CEO received kr4.5m in compensation for the year ending . That seems pretty reasonable, especially given its below the median for similar sized companies. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. I'd also argue reasonable pay levels attest to good decision making more generally.

Should You Add Protector Forsikring To Your Watchlist?

Protector Forsikring's earnings have taken off like any random crypto-currency did, back in 2017. Just as heartening; insiders both own and are buying more stock. Because of the potential that it has reached an inflection point, I'd suggest Protector Forsikring belongs on the top of your watchlist. Still, you should learn about the 1 warning sign we've spotted with Protector Forsikring .

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Protector Forsikring, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:PROT

Protector Forsikring

Operates as a non-life insurance company, provides various insurance products to the commercial and public sectors, and the grouped insurance schemes markets in Norway, Denmark, Sweden, the United Kingdom, and Finland.

Solid track record with excellent balance sheet.