Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:1890

Discovering February 2025's Undiscovered Gems with Strong Potential

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a volatile landscape marked by fluctuating corporate earnings and geopolitical tensions, the small-cap sector faces unique challenges and opportunities. With the Federal Reserve holding rates steady amid persistent inflation concerns, investors are keenly observing economic indicators that could impact small-cap companies. In this environment, identifying stocks with strong fundamentals and growth potential becomes crucial for uncovering undiscovered gems that may thrive despite broader market uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Canal Shipping Agencies | NA | 8.92% | 22.01% | ★★★★★★ |

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Suez Canal Company for Technology Settling (S.A.E) | NA | 22.31% | 13.60% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| SALUS Ljubljana d. d | 13.55% | 13.11% | 9.95% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Arab Banking Corporation (B.S.C.) | 213.15% | 18.58% | 29.63% | ★★★★☆☆ |

| Invest Bank | 135.69% | 11.07% | 18.67% | ★★★★☆☆ |

| Practic | NA | 3.63% | 6.85% | ★★★★☆☆ |

| Jiangsu Aisen Semiconductor MaterialLtd | 12.19% | 14.60% | 12.10% | ★★★★☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

Medistim (OB:MEDI)

Simply Wall St Value Rating: ★★★★★★

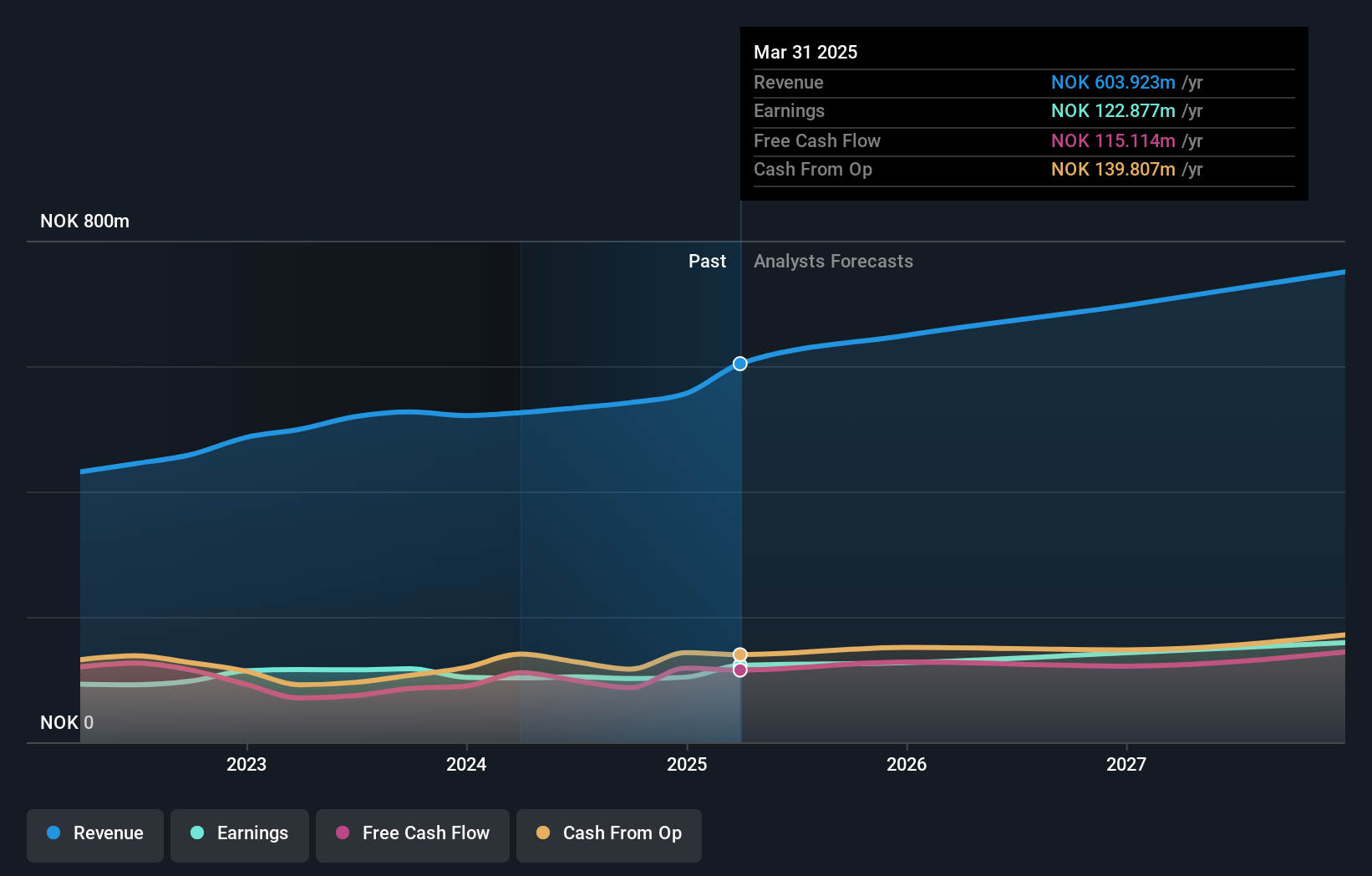

Overview: Medistim ASA is a company that specializes in developing, producing, servicing, leasing, and distributing medical devices for cardiac and vascular surgery across the United States, Europe, Asia, and other international markets with a market cap of NOK2.93 billion.

Operations: Medistim generates revenue primarily from its own products, contributing NOK459.38 million, and third-party products, adding NOK87.70 million.

Medistim, a nimble player in the medical equipment sector, is debt-free and trades at a price-to-earnings ratio of 28.7x, which is below the industry average of 32.9x. Despite experiencing negative earnings growth of -13.3% over the past year, its forecasted annual earnings growth stands at 4.05%. The company recently launched the PATENT study to explore clinical benefits and long-term prognostic value using TTFM and HFUS for bypass surgeries, targeting peripheral artery disease treatment—a market with over 500,000 procedures annually. Medistim’s strategic focus on innovation could enhance its competitive edge in key markets like the United States.

- Navigate through the intricacies of Medistim with our comprehensive health report here.

Assess Medistim's past performance with our detailed historical performance reports.

China Kepei Education Group (SEHK:1890)

Simply Wall St Value Rating: ★★★★☆☆

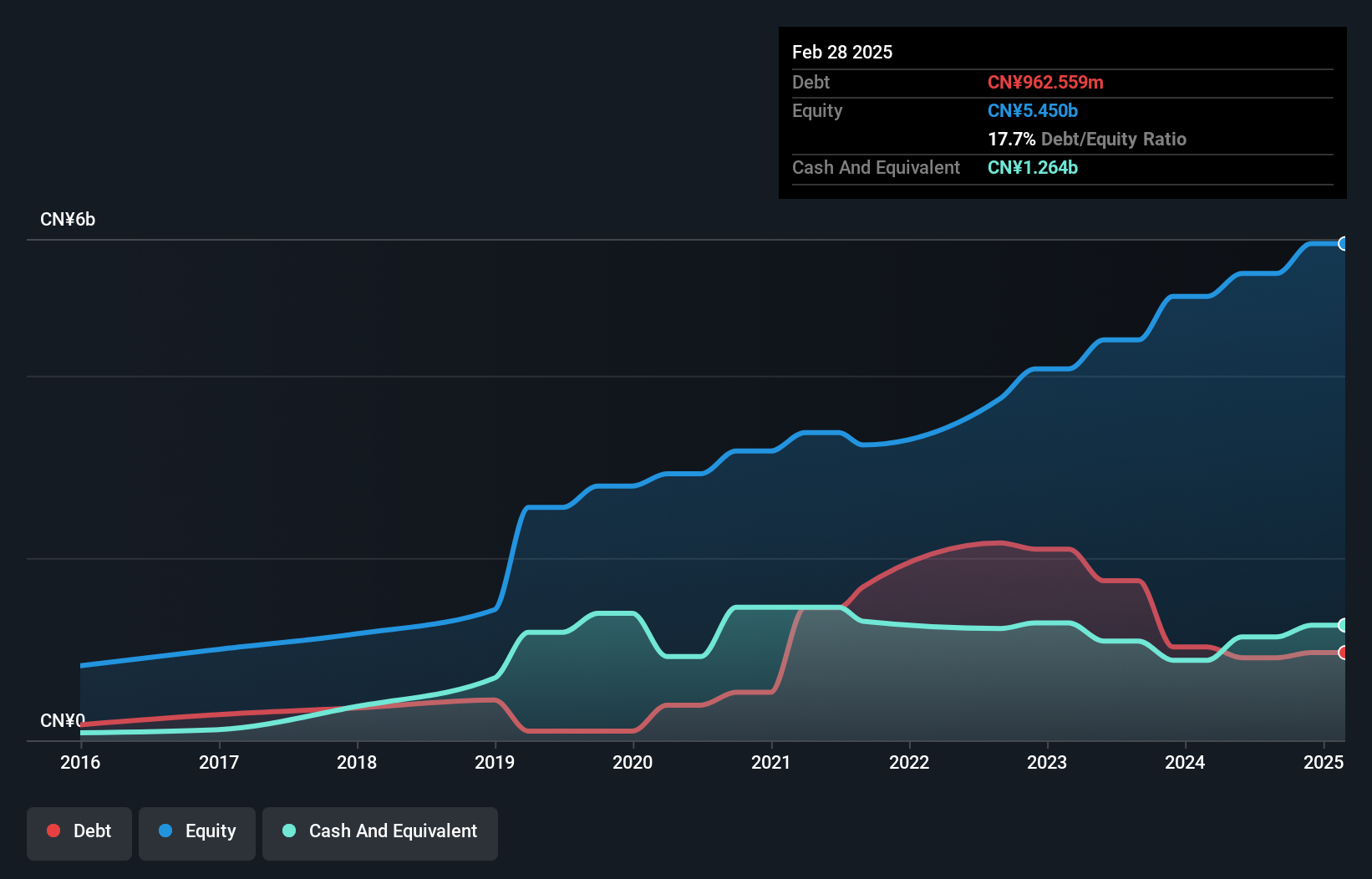

Overview: China Kepei Education Group Limited is an investment holding company that offers private vocational education services with a focus on profession-oriented and vocational training in the People’s Republic of China, with a market capitalization of approximately HK$3.02 billion.

Operations: The primary revenue stream for China Kepei Education Group comes from the provision of education services, generating approximately CN¥1.69 billion. The company's financial performance is characterized by its net profit margin, which reflects the efficiency of its operations.

Kepei Education, a smaller player in the education sector, seems to be gaining traction with its recent performance. Their earnings grew by 11.4% over the past year, surpassing the industry average of 5.5%. Net income reached CNY 827.85 million for the year ending August 2024, up from CNY 743.3 million previously. The company is trading at a significant discount of 76.9% below estimated fair value and offers a proposed dividend of HKD 0.06 per share for shareholders' approval in February 2025, indicating potential value for investors seeking growth and income opportunities within this space.

WUS Printed Circuit (TWSE:2316)

Simply Wall St Value Rating: ★★★★☆☆

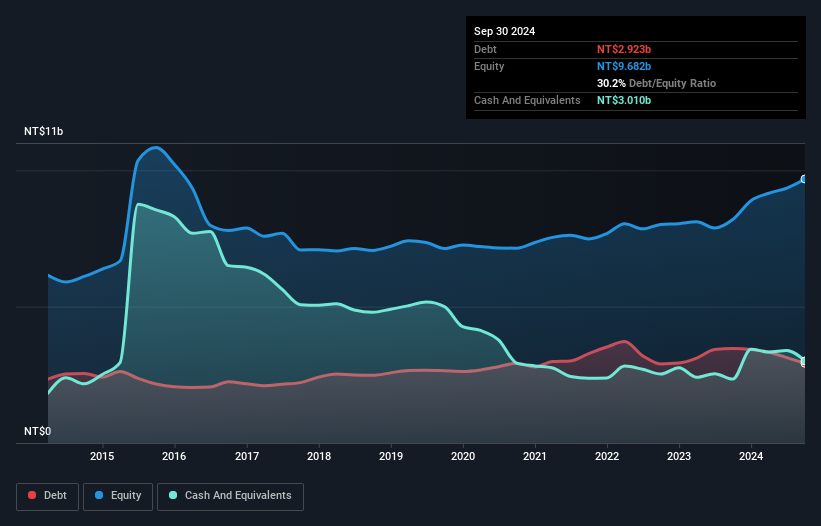

Overview: WUS Printed Circuit Co., Ltd. and its subsidiaries are engaged in the manufacturing, processing, assembly, and sale of double-sided and multi-layer printed circuit boards across Taiwan, Asia, North America, Europe, and other international markets with a market capitalization of NT$8.94 billion.

Operations: WUS Printed Circuit generates revenue primarily from the manufacturing and trading of printed circuit boards, contributing NT$2.12 billion, and the assembly and trading of PCB/light products, adding NT$1.24 billion.

WUS Printed Circuit, a small player in the electronics sector, has recently showcased impressive financial metrics. The company reported a notable net income increase to TWD 189 million for Q3 2024, up from TWD 124 million the previous year. Its earnings per share also rose significantly to TWD 1.04 from TWD 0.68, reflecting robust profitability despite sales dipping slightly to TWD 856 million from last year's TWD 887 million. With a price-to-earnings ratio of just 6.9x compared to the market's average of 20.6x and reduced debt-to-equity ratio over five years, WUS seems well-positioned within its industry context.

- Click to explore a detailed breakdown of our findings in WUS Printed Circuit's health report.

Understand WUS Printed Circuit's track record by examining our Past report.

Key Takeaways

- Explore the 4663 names from our Undiscovered Gems With Strong Fundamentals screener here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1890

China Kepei Education Group

An investment holding company, provides private vocational education services focusing on profession-oriented and vocational education in the People’s Republic of China.

Good value with adequate balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor