Advertisement

- Norway

- /

- Energy Services

- /

- OB:REACH

Reach Subsea's (OB:REACH) Shareholders May Want To Dig Deeper Than Statutory Profit

The stock price didn't jump after Reach Subsea ASA (OB:REACH) posted decent earnings last week. Our analysis showed that there are some concerning factors in the earnings that investors may be cautious of.

View our latest analysis for Reach Subsea

Examining Cashflow Against Reach Subsea's Earnings

Many investors haven't heard of the accrual ratio from cashflow, but it is actually a useful measure of how well a company's profit is backed up by free cash flow (FCF) during a given period. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

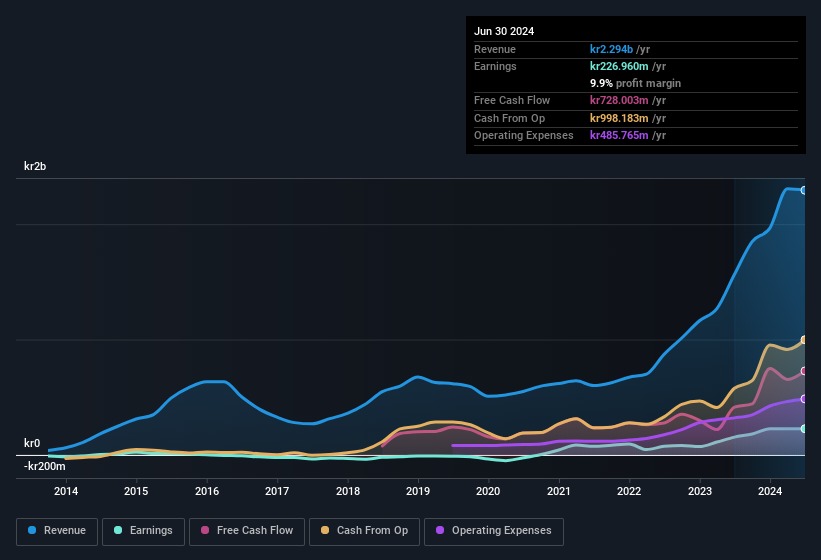

For the year to June 2024, Reach Subsea had an accrual ratio of -0.72. That indicates that its free cash flow quite significantly exceeded its statutory profit. To wit, it produced free cash flow of kr728m during the period, dwarfing its reported profit of kr227.0m. Reach Subsea's free cash flow improved over the last year, which is generally good to see. However, that's not the end of the story. We can look at how unusual items in the profit and loss statement impacted its accrual ratio, as well as explore how dilution is impacting shareholders negatively.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. As it happens, Reach Subsea issued 6.4% more new shares over the last year. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Reach Subsea's historical EPS growth by clicking on this link.

A Look At The Impact Of Reach Subsea's Dilution On Its Earnings Per Share (EPS)

As you can see above, Reach Subsea has been growing its net income over the last few years, with an annualized gain of 204% over three years. In comparison, earnings per share only gained 70% over the same period. And at a glance the 47% gain in profit over the last year impresses. On the other hand, earnings per share are only up 8.0% in that time. And so, you can see quite clearly that dilution is influencing shareholder earnings.

In the long term, earnings per share growth should beget share price growth. So it will certainly be a positive for shareholders if Reach Subsea can grow EPS persistently. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

How Do Unusual Items Influence Profit?

Surprisingly, given Reach Subsea's accrual ratio implied strong cash conversion, its paper profit was actually boosted by kr30m in unusual items. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. And that's as you'd expect, given these boosts are described as 'unusual'. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

Our Take On Reach Subsea's Profit Performance

Summing up, Reach Subsea's accrual ratio suggests that its statutory earnings are well matched by cash flow while its unusual items boosted the profit in a way that might not be repeated. Meanwhile, the dilution was a negative for shareholders. Based on these factors, it's hard to tell if Reach Subsea's profits are a reasonable reflection of its underlying profitability. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. At Simply Wall St, we found 4 warning signs for Reach Subsea and we think they deserve your attention.

In this article we've looked at a number of factors that can impair the utility of profit numbers, as a guide to a business. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:REACH

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|47.8% undervalued

TO

Community Contributor