Advertisement

- Norway

- /

- Oil and Gas

- /

- OB:OET

Growth Investors: Industry Analysts Just Upgraded Their Okeanis Eco Tankers Corp. (OB:OET) Revenue Forecasts By 11%

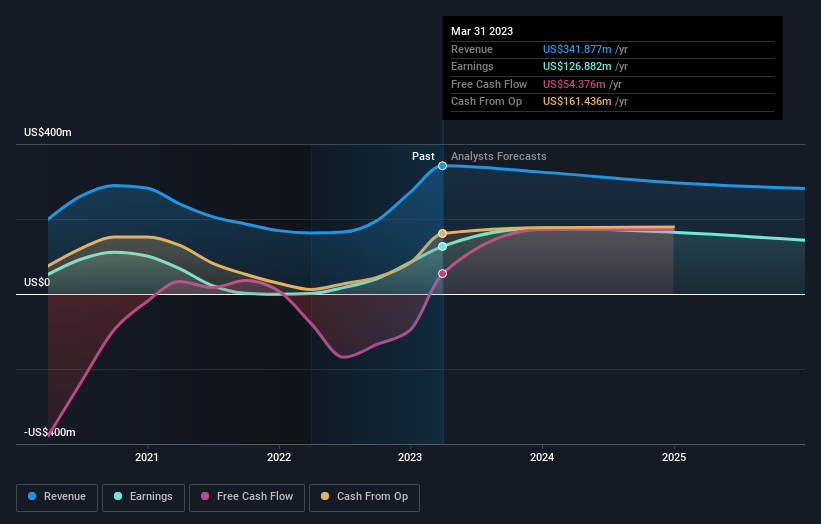

Celebrations may be in order for Okeanis Eco Tankers Corp. (OB:OET) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The revenue forecast for this year has experienced a facelift, with analysts now much more optimistic on its sales pipeline. Investor sentiment seems to be improving too, with the share price up 5.3% to kr250 over the past 7 days. Could this big upgrade push the stock even higher?

Following the upgrade, the consensus from twin analysts covering Okeanis Eco Tankers is for revenues of US$325m in 2023, implying a measurable 4.9% decline in sales compared to the last 12 months. Prior to the latest estimates, the analysts were forecasting revenues of US$294m in 2023. The consensus has definitely become more optimistic, showing a decent improvement in revenue forecasts.

See our latest analysis for Okeanis Eco Tankers

We'd point out that there was no major changes to their price target of US$28.97, suggesting the latest estimates were not enough to shift their view on the value of the business. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. The most optimistic Okeanis Eco Tankers analyst has a price target of US$326 per share, while the most pessimistic values it at US$293. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely differing views on what kind of performance this business can generate. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. One more thing stood out to us about these estimates, and it's the idea that Okeanis Eco Tankers' decline is expected to accelerate, with revenues forecast to fall at an annualised rate of 6.5% to the end of 2023. This tops off a historical decline of 0.1% a year over the past three years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue shrink 12% per year. So it's pretty clear that, although revenues are shrinking, at least Okeanis Eco Tankers'revenues are expected to decline at a slower rate than the wider industry.

The Bottom Line

The highlight for us was that analysts increased their revenue forecasts for Okeanis Eco Tankers this year. They're also forecasting for revenues to perform better than companies in the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Okeanis Eco Tankers.

Unsatisfied? We have analyst estimates for Okeanis Eco Tankers going out to 2025, and you can see them free on our platform here.

Another thing to consider is whether management and directors have been buying or selling stock recently. We provide an overview of all open market stock trades for the last twelve months on our platform, here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:OET

Okeanis Eco Tankers

A shipping company, owns and operates tanker vessels worldwide.

Good value with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor