Advertisement

- Norway

- /

- Energy Services

- /

- OB:ODL

Odfjell Drilling Ltd. (OB:ODL) Just Reported And Analysts Have Been Lifting Their Price Targets

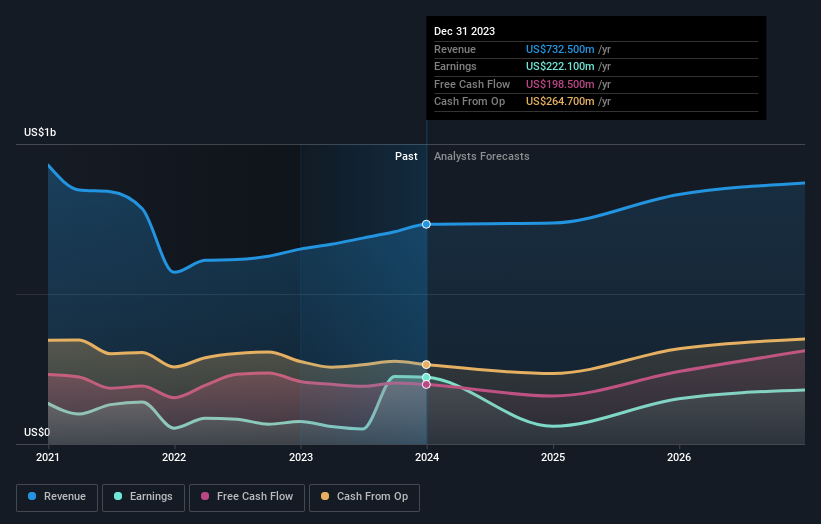

Investors in Odfjell Drilling Ltd. (OB:ODL) had a good week, as its shares rose 6.9% to close at kr44.15 following the release of its yearly results. Odfjell Drilling reported US$733m in revenue, roughly in line with analyst forecasts, although statutory earnings per share (EPS) of US$0.94 beat expectations, being 3.5% higher than what the analysts expected. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

See our latest analysis for Odfjell Drilling

Taking into account the latest results, Odfjell Drilling's four analysts currently expect revenues in 2024 to be US$736.6m, approximately in line with the last 12 months. Statutory earnings per share are forecast to crater 73% to US$0.25 in the same period. Before this earnings report, the analysts had been forecasting revenues of US$716.4m and earnings per share (EPS) of US$0.22 in 2024. So it seems there's been a definite increase in optimism about Odfjell Drilling's future following the latest results, with a nice gain to the earnings per share forecasts in particular.

It will come as no surprise to learn that the analysts have increased their price target for Odfjell Drilling 9.3% to kr57.06on the back of these upgrades. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Odfjell Drilling analyst has a price target of kr64.71 per share, while the most pessimistic values it at kr45.04. With such a wide range in price targets, analysts are almost certainly betting on widely divergent outcomes in the underlying business. With this in mind, we wouldn't rely too heavily the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Odfjell Drilling's past performance and to peers in the same industry. It's also worth noting that the years of declining revenue look to have come to an end, with the forecast stauing flat to the end of 2024. Historically, Odfjell Drilling's top line has shrunk approximately 3.5% annually over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 7.5% per year. Although Odfjell Drilling's revenues are expected to improve, it seems that it is still expected to grow slower than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Odfjell Drilling's earnings potential next year. Fortunately, they also upgraded their revenue estimates, although our data indicates it is expected to perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for Odfjell Drilling going out to 2026, and you can see them free on our platform here.

Even so, be aware that Odfjell Drilling is showing 3 warning signs in our investment analysis , and 1 of those is potentially serious...

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:ODL

Odfjell Drilling

Engages in owning and operating mobile offshore drilling units primarily in Norway and Namibia.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.7% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Pagaya Technologies ·

The "Rate Cut" Supercycle Winner – Profitable & Accelerating

Fair Value:US$170.685.9% undervalued

1 followerusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Archer Aviation ·

The Industrialist of the Skies – Scaling with "Automotive DNA

Fair Value:US$16.3254.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

111 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative