- Norway

- /

- Energy Services

- /

- OB:BWO

Earnings Miss: BW Offshore Limited Missed EPS By 53% And Analysts Are Revising Their Forecasts

BW Offshore Limited (OB:BWO) missed earnings with its latest quarterly results, disappointing overly-optimistic forecasters. It wasn't a great result overall - while revenue fell marginally short of analyst estimates at US$195m, statutory earnings missed forecasts by an incredible 53%, coming in at just US$0.07 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

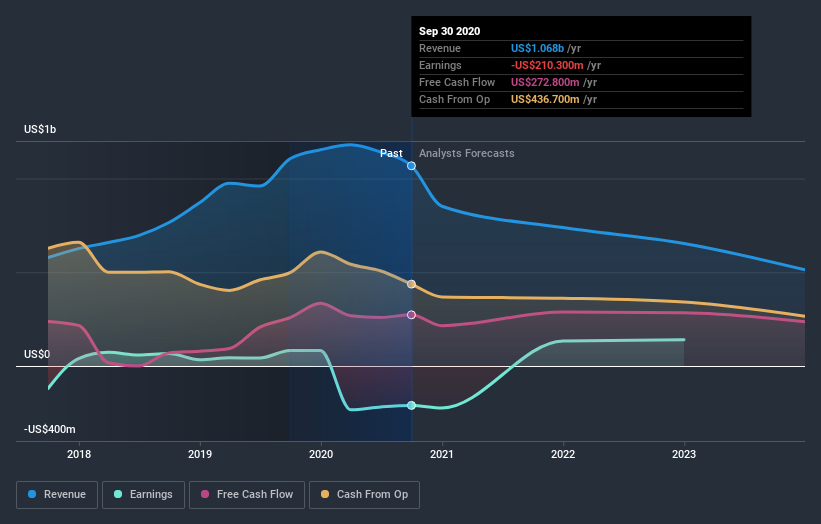

Check out our latest analysis for BW Offshore

Following the recent earnings report, the consensus from five analysts covering BW Offshore is for revenues of US$738.2m in 2021, implying a substantial 31% decline in sales compared to the last 12 months. BW Offshore is also expected to turn profitable, with statutory earnings of US$0.67 per share. In the lead-up to this report, the analysts had been modelling revenues of US$749.0m and earnings per share (EPS) of US$0.70 in 2021. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analysts did make a minor downgrade to their earnings per share forecasts.

The consensus price target held steady at US$5.01, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on BW Offshore, with the most bullish analyst valuing it at US$49.61 and the most bearish at US$36.84 per share. So we wouldn't be assigning too much credibility to analyst price targets in this case, because there are clearly some widely different views on what kind of performance this business can generate. As a result it might not be a great idea to make decisions based on the consensus price target, which is after all just an average of this wide range of estimates.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the BW Offshore's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast revenue decline of 31%, a significant reduction from annual growth of 11% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 0.4% next year. It's pretty clear that BW Offshore's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. On the plus side, there were no major changes to revenue estimates; although forecasts imply revenues will perform worse than the wider industry. The consensus price target held steady at US$5.01, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for BW Offshore going out to 2023, and you can see them free on our platform here..

We don't want to rain on the parade too much, but we did also find 2 warning signs for BW Offshore that you need to be mindful of.

When trading BW Offshore or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if BW Offshore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About OB:BWO

BW Offshore

Engages in the engineering of offshore production solutions in the Americas, Europe, Africa, Asia, and the Pacific.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Community Narratives