Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Quantafuel ASA (OB:QFUEL) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Quantafuel

How Much Debt Does Quantafuel Carry?

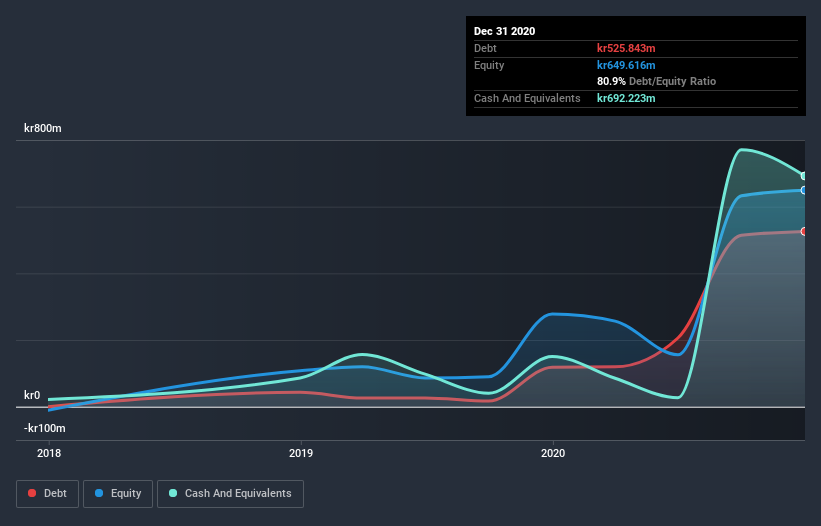

As you can see below, at the end of December 2020, Quantafuel had kr525.8m of debt, up from kr118.5m a year ago. Click the image for more detail. But on the other hand it also has kr692.2m in cash, leading to a kr166.4m net cash position.

How Healthy Is Quantafuel's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Quantafuel had liabilities of kr147.4m due within 12 months and liabilities of kr705.1m due beyond that. Offsetting these obligations, it had cash of kr692.2m as well as receivables valued at kr17.6m due within 12 months. So it has liabilities totalling kr142.7m more than its cash and near-term receivables, combined.

Given Quantafuel has a market capitalization of kr6.91b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Quantafuel also has more cash than debt, so we're pretty confident it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Quantafuel can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Over 12 months, Quantafuel reported revenue of kr8.4m, which is a gain of 1,588%, although it did not report any earnings before interest and tax. That's virtually the hole-in-one of revenue growth!

So How Risky Is Quantafuel?

Statistically speaking companies that lose money are riskier than those that make money. And we do note that Quantafuel had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through kr337m of cash and made a loss of kr495m. With only kr166.4m on the balance sheet, it would appear that its going to need to raise capital again soon. Importantly, Quantafuel's revenue growth is hot to trot. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Quantafuel you should be aware of, and 1 of them is significant.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you’re looking to trade Quantafuel, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Quantafuel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About OB:QFUEL

Quantafuel

Quantafuel ASA, a technology-based energy company engages in converting plastic waste to low-carbon synthetic oil products replacing virgin oil products in Norway.

High growth potential and overvalued.

Similar Companies

Market Insights

Community Narratives