Here's Why It's Unlikely That Philly Shipyard ASA's (OB:PHLY) CEO Will See A Pay Rise This Year

Key Insights

- Philly Shipyard's Annual General Meeting to take place on 15th of April

- Salary of US$452.0k is part of CEO Steinar Nerbovik's total remuneration

- The overall pay is 117% above the industry average

- Philly Shipyard's EPS declined by 89% over the past three years while total shareholder loss over the past three years was 45%

Shareholders will probably not be too impressed with the underwhelming results at Philly Shipyard ASA (OB:PHLY) recently. Shareholders can take the chance to hold the board and management accountable for the unsatisfactory performance at the next AGM on 15th of April. This will be also be a chance where they can challenge the board on company direction and vote on resolutions such as executive remuneration. From our analysis, we think CEO compensation may need a review in light of the recent performance.

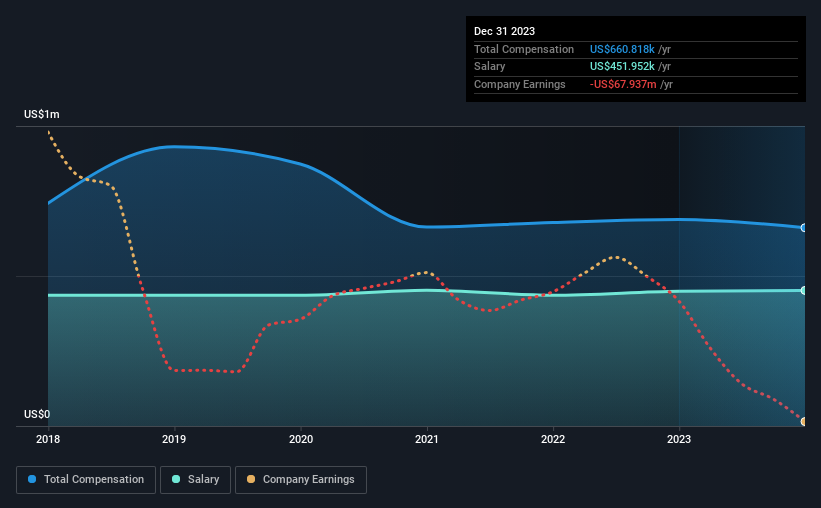

Check out our latest analysis for Philly Shipyard

Comparing Philly Shipyard ASA's CEO Compensation With The Industry

According to our data, Philly Shipyard ASA has a market capitalization of kr442m, and paid its CEO total annual compensation worth US$661k over the year to December 2023. We note that's a small decrease of 4.0% on last year. We note that the salary portion, which stands at US$452.0k constitutes the majority of total compensation received by the CEO.

On comparing similar-sized companies in the Norwegian Machinery industry with market capitalizations below kr2.1b, we found that the median total CEO compensation was US$304k. Hence, we can conclude that Steinar Nerbovik is remunerated higher than the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$452k | US$449k | 68% |

| Other | US$209k | US$239k | 32% |

| Total Compensation | US$661k | US$688k | 100% |

Talking in terms of the industry, salary represented approximately 85% of total compensation out of all the companies we analyzed, while other remuneration made up 15% of the pie. It's interesting to note that Philly Shipyard allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Philly Shipyard ASA's Growth Numbers

Over the last three years, Philly Shipyard ASA has shrunk its earnings per share by 89% per year. It achieved revenue growth of 13% over the last year.

Overall this is not a very positive result for shareholders. There's no doubt that the silver lining is that revenue is up. But it isn't sufficiently fast growth to overlook the fact that EPS has gone backwards over three years. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Philly Shipyard ASA Been A Good Investment?

Few Philly Shipyard ASA shareholders would feel satisfied with the return of -45% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

Not only have shareholders not seen a favorable return on their investment, but the business hasn't performed well either. Few shareholders would be willing to award the CEO with a pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. That's why we did our research, and identified 3 warning signs for Philly Shipyard (of which 1 is concerning!) that you should know about in order to have a holistic understanding of the stock.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

If you're looking to trade Philly Shipyard, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:PHLY

Philly Shipyard

Operates a commercial shipyard that builds and repairs vessels for the United States Jones Act market and government.

Flawless balance sheet slight.

Market Insights

Community Narratives