Eqva (OB:EQVA) hikes 11% this week, taking three-year gains to 57%

It's nice to see the Eqva ASA (OB:EQVA) share price up 11% in a week.

The recent uptick of 11% could be a positive sign of things to come, so let's take a look at historical fundamentals.

View our latest analysis for Eqva

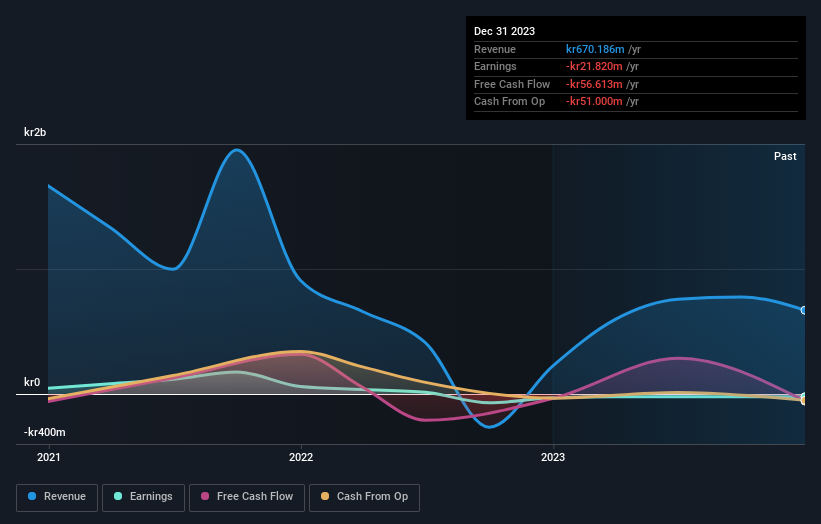

Eqva wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. When a company doesn't make profits, we'd generally hope to see good revenue growth. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

Over the last three years, Eqva's revenue dropped 41% per year. That's definitely a weaker result than most pre-profit companies report. The swift share price decline at an annual compound rate of 21%, reflects this weak fundamental performance. Never forget that loss making companies with falling revenue can and do cause losses for everyday investors. There is a good reason that investors often describe buying a sharply falling stock price as 'trying to catch a falling knife'. Think about it.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

If you are thinking of buying or selling Eqva stock, you should check out this FREE detailed report on its balance sheet.

What About The Total Shareholder Return (TSR)?

We'd be remiss not to mention the difference between Eqva's total shareholder return (TSR) and its share price return. The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. Dividends have been really beneficial for Eqva shareholders, and that cash payout contributed to why its TSR of 57%, over the last 3 years, is better than the share price return.

A Different Perspective

We're pleased to report that Eqva shareholders have received a total shareholder return of 26% over one year. Having said that, the five-year TSR of 31% a year, is even better. It's always interesting to track share price performance over the longer term. But to understand Eqva better, we need to consider many other factors. Like risks, for instance. Every company has them, and we've spotted 2 warning signs for Eqva (of which 1 is significant!) you should know about.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Norwegian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Eqva might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:EQVA

Eqva

Provides technical solutions and services to maritime and land based industries in Norway and internationally.

Good value with adequate balance sheet.