Advertisement

Cambi ASA (OB:CAMBI) Analysts Are Pretty Bullish On The Stock After Recent Results

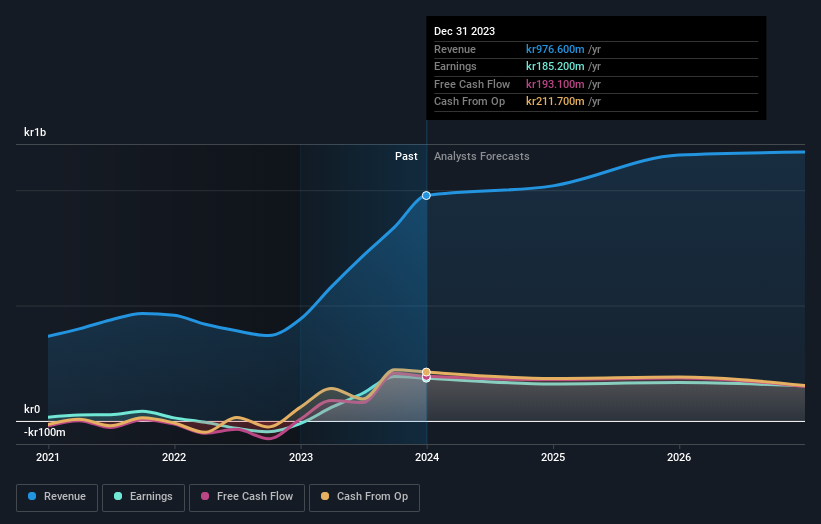

Last week, you might have seen that Cambi ASA (OB:CAMBI) released its yearly result to the market. The early response was not positive, with shares down 4.3% to kr16.80 in the past week. Overall the results were a little better than the analyst was expecting, with revenues beating forecasts by 3.7%to hit kr977m. Earnings are an important time for investors, as they can track a company's performance, look at what the analyst is forecasting for next year, and see if there's been a change in sentiment towards the company. We thought readers would find it interesting to see the analyst latest (statutory) post-earnings forecasts for next year.

View our latest analysis for Cambi

Taking into account the latest results, the most recent consensus for Cambi from solitary analyst is for revenues of kr1.02b in 2024. If met, it would imply a reasonable 4.3% increase on its revenue over the past 12 months. Yet prior to the latest earnings, the analyst had been anticipated revenues of kr994.7m and earnings per share (EPS) of kr0.97 in 2024. The thing that stands out most is that, while there's been a slight bump in revenue estimates, the consensus no longer provides an EPS estimate. This impliesthat revenue is more important following the latest results.

The average price target rose 67% to kr20.00, with the analyst clearly having become more optimistic about Cambi'sprospects following these results.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that Cambi's revenue growth is expected to slow, with the forecast 4.3% annualised growth rate until the end of 2024 being well below the historical 22% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 11% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Cambi.

The Bottom Line

The highlight for us was that the analyst increased their revenue forecasts for Cambi next year. Fortunately, they also upgraded their revenue estimates, although our data indicates it is expected to perform worse than the wider industry. We note an upgrade to the price target, suggesting that the analyst believes the intrinsic value of the business is likely to improve over time.

One Cambi broker/analyst has provided estimates out to 2026, which can be seen for free on our platform here.

However, before you get too enthused, we've discovered 1 warning sign for Cambi that you should be aware of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OB:CAMBI

Cambi

Provides thermal hydrolysis solutions for sewage sludge and organic waste management in Europe, the Americas, Asia, Africa, and Oceania.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor