These Analysts Just Made A Meaningful Downgrade To Their SpareBank 1 BV (OB:SBVG) EPS Forecasts

Market forces rained on the parade of SpareBank 1 BV (OB:SBVG) shareholders today, when the analysts downgraded their forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with analysts seeing grey clouds on the horizon.

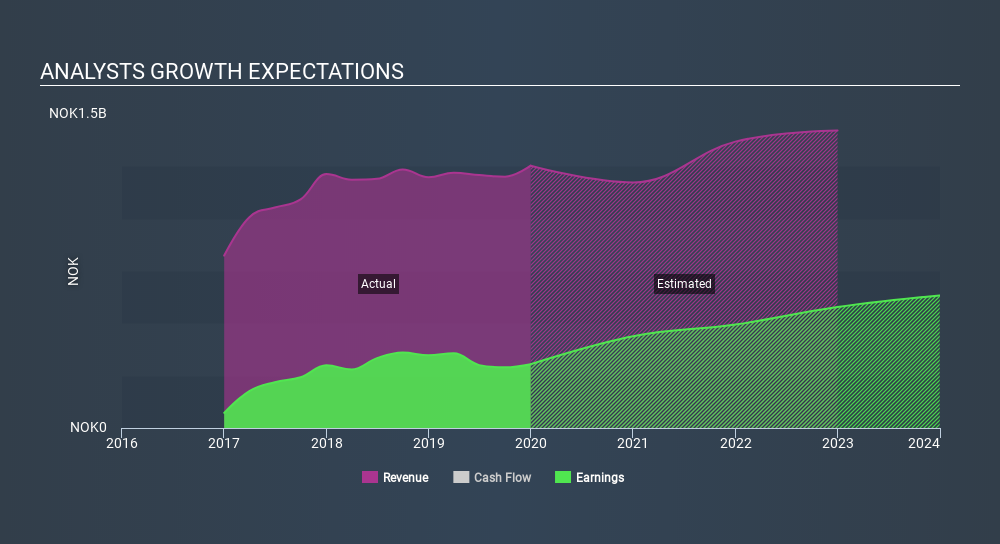

After the downgrade, the consensus from SpareBank 1 BV's dual analysts is for revenues of kr1.2b in 2020, which would reflect a measurable 6.4% decline in sales compared to the last year of performance. Statutory earnings per share are supposed to drop 20% to kr3.87 in the same period. Before this latest update, the analysts had been forecasting revenues of kr1.4b and earnings per share (EPS) of kr5.15 in 2020. Indeed, we can see that the analysts are a lot more bearish about SpareBank 1 BV's prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

View our latest analysis for SpareBank 1 BV

The consensus price target fell 8.3% to kr44.00, with the weaker earnings outlook clearly leading analyst valuation estimates. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic SpareBank 1 BV analyst has a price target of kr51.00 per share, while the most pessimistic values it at kr37.00. Analysts definitely have varying views on the business, but the spread of estimates is not wide enough in our view to suggest that extreme outcomes could await SpareBank 1 BV shareholders.

Of course, another way to look at these forecasts is to place them into context against the industry itself. These estimates imply that sales are expected to slow, with a forecast revenue decline of 6.4%, a significant reduction from annual growth of 16% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 2.7% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - SpareBank 1 BV is expected to lag the wider industry.

The Bottom Line

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for SpareBank 1 BV. Unfortunately analysts also downgraded their revenue estimates, and industry data suggests that SpareBank 1 BV's revenues are expected to grow slower than the wider market. After such a stark change in sentiment from analysts, we'd understand if readers now felt a bit wary of SpareBank 1 BV.

There might be good reason for analyst bearishness towards SpareBank 1 BV, like concerns around earnings quality. Learn more, and discover the 2 other risks we've identified, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About OB:SOON

SpareBank 1 Sørøst-Norge

Provides various banking products and services for private and corporate customers in Norway.

Adequate balance sheet average dividend payer.