- South Korea

- /

- Semiconductors

- /

- KOSDAQ:A166090

3 Growth Companies Insiders Are Betting On

Reviewed by Simply Wall St

In the wake of recent global market developments, U.S. stocks have been marching toward record highs, driven by optimism around potential trade deals and enthusiasm for artificial intelligence investments. With growth stocks outperforming value shares for the first time this year, investors are increasingly focusing on companies that insiders are betting on as a sign of confidence in future performance. In such a climate, high insider ownership can be seen as an indicator of alignment between company leadership and shareholder interests, making these growth companies particularly noteworthy.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 20.5% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 36.6% |

| Pharma Mar (BME:PHM) | 11.9% | 55.1% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 135% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

| HANA Micron (KOSDAQ:A067310) | 18.2% | 119.4% |

| Findi (ASX:FND) | 35.8% | 110.7% |

We'll examine a selection from our screener results.

PostNL (ENXTAM:PNL)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PostNL N.V. offers postal and logistics services to businesses and consumers across the Netherlands, Europe, and internationally, with a market cap of €482.03 million.

Operations: PostNL generates revenue through its postal and logistics services provided to businesses and consumers within the Netherlands, throughout Europe, and globally.

Insider Ownership: 35.6%

Earnings Growth Forecast: 44.9% p.a.

PostNL's earnings are forecast to grow significantly at 44.9% annually, outpacing the Dutch market's 14.5%. Despite trading at a substantial discount to its estimated fair value, it faces challenges with high debt levels and slower revenue growth of 2.2% per year compared to the market's 8.3%. Recent financial results showed increased sales but ongoing losses, with Q4 guidance indicating normalized EBIT around €53 million and comprehensive income approximately €38 million for 2024.

- Navigate through the intricacies of PostNL with our comprehensive analyst estimates report here.

- Our comprehensive valuation report raises the possibility that PostNL is priced lower than what may be justified by its financials.

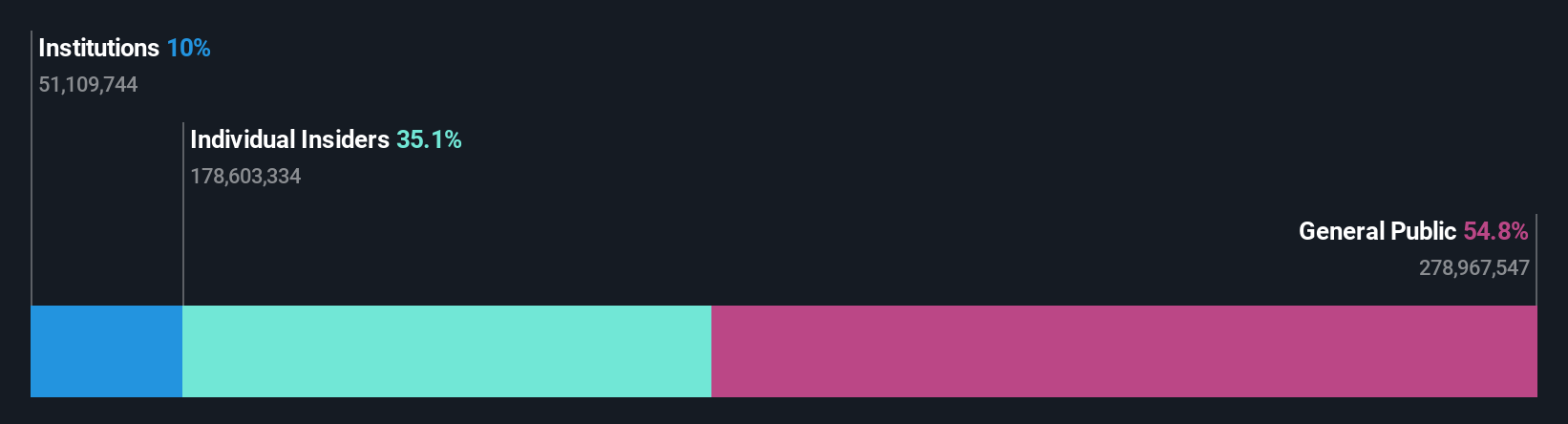

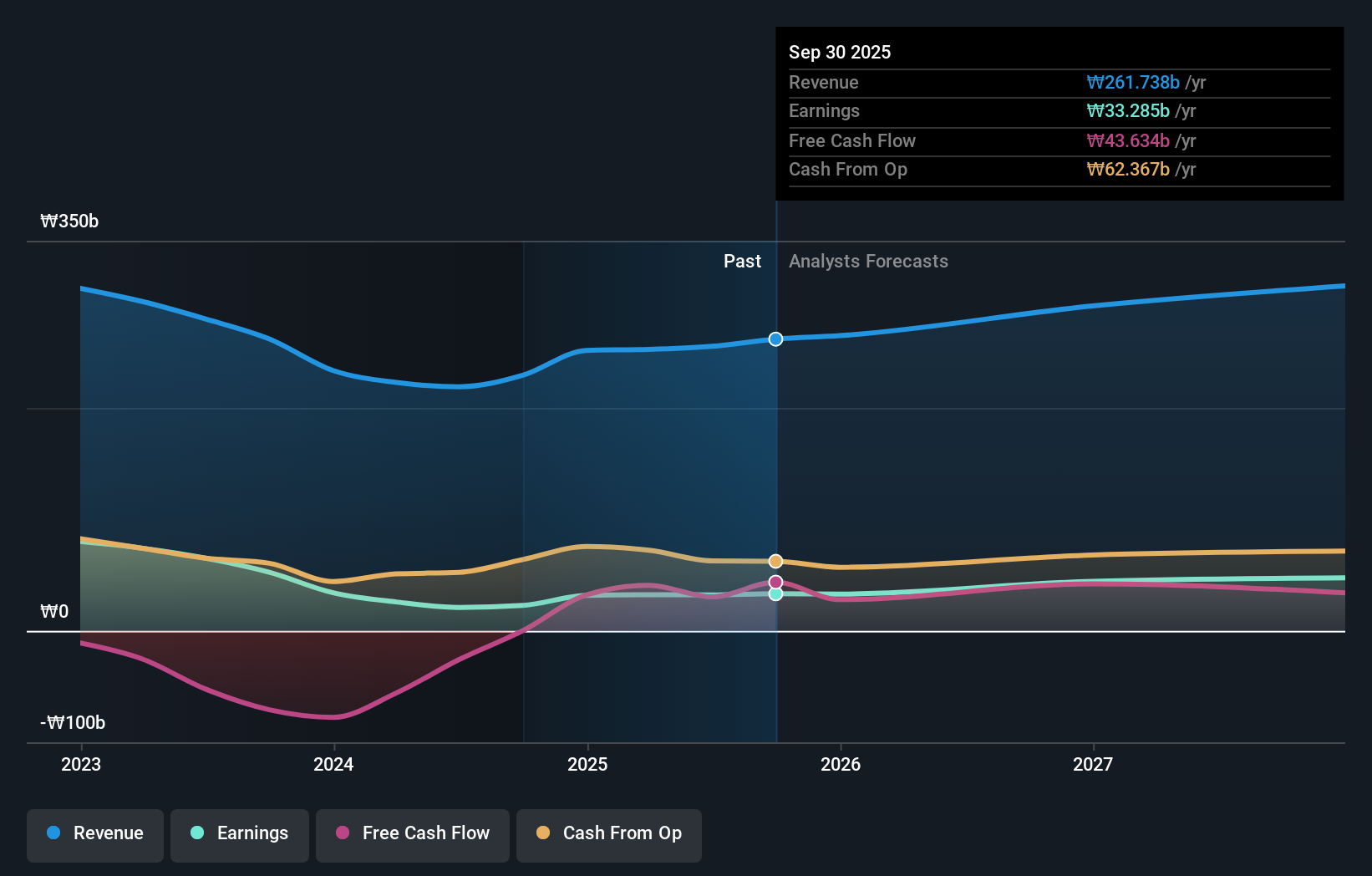

Hana Materials (KOSDAQ:A166090)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hana Materials Inc. manufactures and sells silicon electrodes and rings in South Korea, with a market cap of approximately ₩517.41 billion.

Operations: Revenue segments for the company include manufacturing and selling silicon electrodes and rings in South Korea.

Insider Ownership: 12.9%

Earnings Growth Forecast: 48.2% p.a.

Hana Materials is poised for strong growth, with earnings expected to rise 48.22% annually, surpassing the Korean market's 27.8%. Revenue growth is forecast at 18.3% per year, outpacing the market average of 9.2%. Despite a high debt level and declining profit margins from last year (20% to 9.9%), it trades slightly below its fair value estimate and has initiated a KRW 5 billion share buyback program to enhance shareholder value and stabilize stock prices.

- Dive into the specifics of Hana Materials here with our thorough growth forecast report.

- Our valuation report unveils the possibility Hana Materials' shares may be trading at a premium.

Dirui IndustrialLtd (SZSE:300396)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Dirui Industrial Co., Ltd. focuses on the research, development, production, and sale of medical inspection products in China, with a market cap of CN¥4.03 billion.

Operations: The company generates revenue primarily from its Medical Instruments segment, amounting to CN¥1.50 billion.

Insider Ownership: 12.2%

Earnings Growth Forecast: 40.5% p.a.

Dirui Industrial Ltd. is positioned for robust growth, with earnings projected to increase by 40.5% annually, outpacing the Chinese market's 25%. Revenue is expected to grow at 35.4% per year, significantly above the market average of 13.3%. Despite a low forecasted Return on Equity of 13.4%, its Price-To-Earnings ratio of 17.2x suggests good value compared to peers and industry standards, although its dividend yield of 3.36% isn't well supported by free cash flows.

- Unlock comprehensive insights into our analysis of Dirui IndustrialLtd stock in this growth report.

- Our valuation report here indicates Dirui IndustrialLtd may be undervalued.

Next Steps

- Gain an insight into the universe of 1482 Fast Growing Companies With High Insider Ownership by clicking here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Hana Materials might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About KOSDAQ:A166090

Hana Materials

Manufactures and sells silicon electrodes and rings in South Korea.

Reasonable growth potential with adequate balance sheet.

Market Insights

Community Narratives