- Netherlands

- /

- Specialty Stores

- /

- ENXTAM:BBED

Increases to CEO Compensation Might Be Put On Hold For Now at Beter Bed Holding N.V. (AMS:BBED)

Shareholders of Beter Bed Holding N.V. (AMS:BBED) will have been dismayed by the negative share price return over the last three years. In addition, the company's per-share earnings growth is not looking good, despite growing revenues. In light of this performance, shareholders will have a chance to question the board in the upcoming AGM on 12 May 2021, where they can impact on future company performance by voting on resolutions, including executive compensation. Here's why we think shareholders should hold off on a raise for the CEO at the moment.

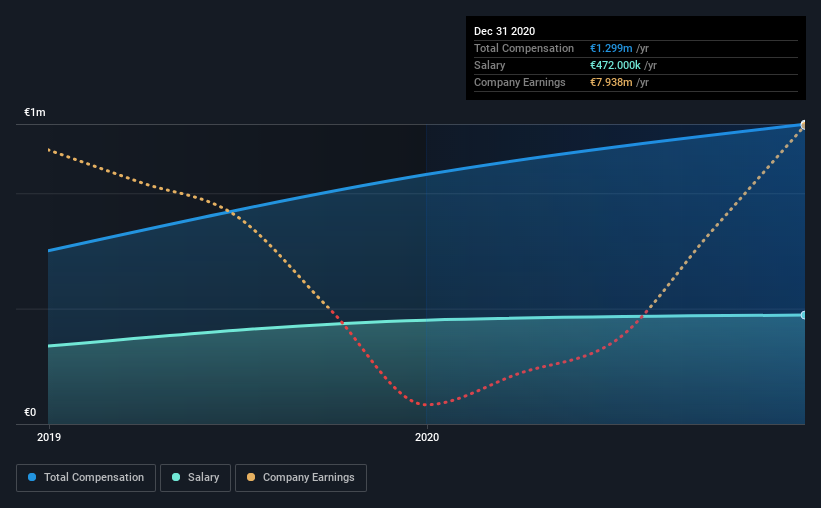

Check out our latest analysis for Beter Bed Holding

How Does Total Compensation For John Kruijssen Compare With Other Companies In The Industry?

Our data indicates that Beter Bed Holding N.V. has a market capitalization of €135m, and total annual CEO compensation was reported as €1.3m for the year to December 2020. Notably, that's an increase of 20% over the year before. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at €472k.

On comparing similar companies from the same industry with market caps ranging from €83m to €333m, we found that the median CEO total compensation was €493k. Accordingly, our analysis reveals that Beter Bed Holding N.V. pays John Kruijssen north of the industry median. What's more, John Kruijssen holds €51k worth of shares in the company in their own name.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | €472k | €450k | 36% |

| Other | €827k | €631k | 64% |

| Total Compensation | €1.3m | €1.1m | 100% |

On an industry level, around 63% of total compensation represents salary and 37% is other remuneration. Beter Bed Holding pays a modest slice of remuneration through salary, as compared to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

Beter Bed Holding N.V.'s Growth

Beter Bed Holding N.V. has reduced its earnings per share by 13% a year over the last three years. In the last year, its revenue is up 19%.

The reduction in EPS, over three years, is arguably concerning. On the other hand, the strong revenue growth suggests the business is growing. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Beter Bed Holding N.V. Been A Good Investment?

The return of -37% over three years would not have pleased Beter Bed Holding N.V. shareholders. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

The loss to shareholders over the past three years is certainly concerning and possibly has something to do with the fact that the company's earnings haven't grown. In the upcoming AGM, shareholders will get the opportunity to discuss any issues with the board, including those related to CEO remuneration and assess if the board's plan is in line with their expectations.

CEO compensation can have a massive impact on performance, but it's just one element. We did our research and spotted 1 warning sign for Beter Bed Holding that investors should look into moving forward.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

If you’re looking to trade Beter Bed Holding, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Beter Bed Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ENXTAM:BBED

Beter Bed Holding

Beter Bed Holding N.V. retails and wholesales bedroom furnishing products in the Netherlands and Belgium.

Flawless balance sheet with moderate growth potential.