- Netherlands

- /

- Professional Services

- /

- ENXTAM:AVTX

Why We're Not Concerned Yet About Avantium N.V.'s (AMS:AVTX) 38% Share Price Plunge

Avantium N.V. (AMS:AVTX) shareholders that were waiting for something to happen have been dealt a blow with a 38% share price drop in the last month. For any long-term shareholders, the last month ends a year to forget by locking in a 52% share price decline.

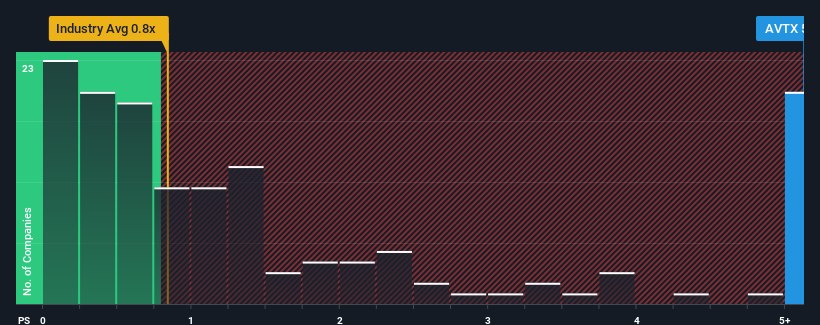

In spite of the heavy fall in price, you could still be forgiven for thinking Avantium is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 5.1x, considering almost half the companies in the Netherlands' Professional Services industry have P/S ratios below 0.7x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Avantium

What Does Avantium's P/S Mean For Shareholders?

Recent times have been advantageous for Avantium as its revenues have been rising faster than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Avantium will help you uncover what's on the horizon.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, Avantium would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered an exceptional 30% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 66% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Looking ahead now, revenue is anticipated to climb by 48% per year during the coming three years according to the four analysts following the company. That's shaping up to be materially higher than the 5.6% per annum growth forecast for the broader industry.

In light of this, it's understandable that Avantium's P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

A significant share price dive has done very little to deflate Avantium's very lofty P/S. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our look into Avantium shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

Having said that, be aware Avantium is showing 3 warning signs in our investment analysis, and 1 of those makes us a bit uncomfortable.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTAM:AVTX

Avantium

A chemical technology company, develops and commercializes renewable chemistry solutions in the Netherlands.

Mediocre balance sheet with limited growth.

Market Insights

Community Narratives