- Malaysia

- /

- Infrastructure

- /

- KLSE:WCEHB

Those who invested in WCE Holdings Berhad (KLSE:WCEHB) five years ago are up 159%

The worst result, after buying shares in a company (assuming no leverage), would be if you lose all the money you put in. But on the bright side, if you buy shares in a high quality company at the right price, you can gain well over 100%. For instance, the price of WCE Holdings Berhad (KLSE:WCEHB) stock is up an impressive 159% over the last five years. Also pleasing for shareholders was the 12% gain in the last three months.

Now it's worth having a look at the company's fundamentals too, because that will help us determine if the long term shareholder return has matched the performance of the underlying business.

See our latest analysis for WCE Holdings Berhad

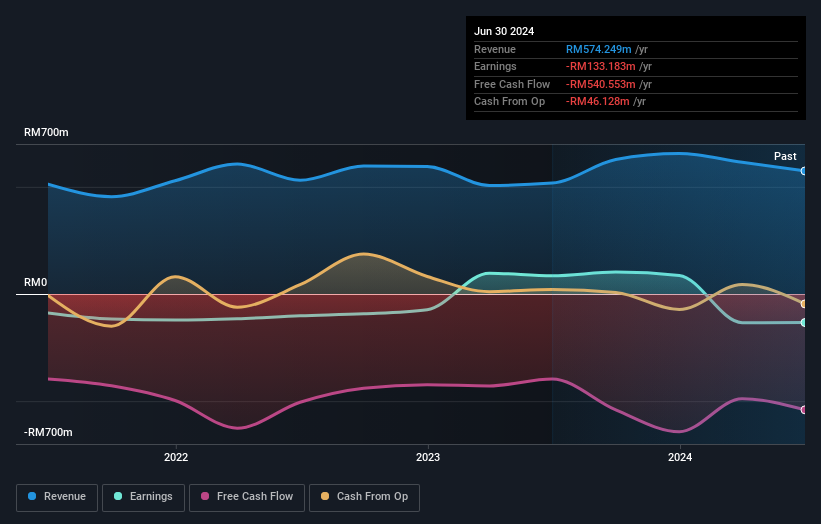

Given that WCE Holdings Berhad didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Shareholders of unprofitable companies usually desire strong revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one would hope for good top-line growth to make up for the lack of earnings.

In the last 5 years WCE Holdings Berhad saw its revenue shrink by 7.2% per year. Given that scenario, we wouldn't have expected the share price to rise 21% per year, but that's what it did. It just goes to show tht the market is forward looking, and it's not always easy to predict the future based on past trends. Still, this situation makes us a little wary of the stock.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

Take a more thorough look at WCE Holdings Berhad's financial health with this free report on its balance sheet.

A Different Perspective

WCE Holdings Berhad shareholders gained a total return of 6.0% during the year. But that return falls short of the market. It's probably a good sign that the company has an even better long term track record, having provided shareholders with an annual TSR of 21% over five years. It's quite possible the business continues to execute with prowess, even as the share price gains are slowing. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For instance, we've identified 2 warning signs for WCE Holdings Berhad (1 is significant) that you should be aware of.

If you are like me, then you will not want to miss this free list of undervalued small caps that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Malaysian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if WCE Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:WCEHB

WCE Holdings Berhad

An investment holding company, engages in the construction, management, and tolling of highway operation in Malaysia.

Minimal with weak fundamentals.

Market Insights

Community Narratives