Earnings Release: Here's Why Analysts Cut Their Pos Malaysia Berhad (KLSE:POS) Price Target To RM1.09

There's been a notable change in appetite for Pos Malaysia Berhad (KLSE:POS) shares in the week since its annual report, with the stock down 10% to RM0.90. It was a pretty bad result overall; while revenues were in line with expectations at RM2.2b, statutory losses exploded to RM0.39 per share. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Pos Malaysia Berhad after the latest results.

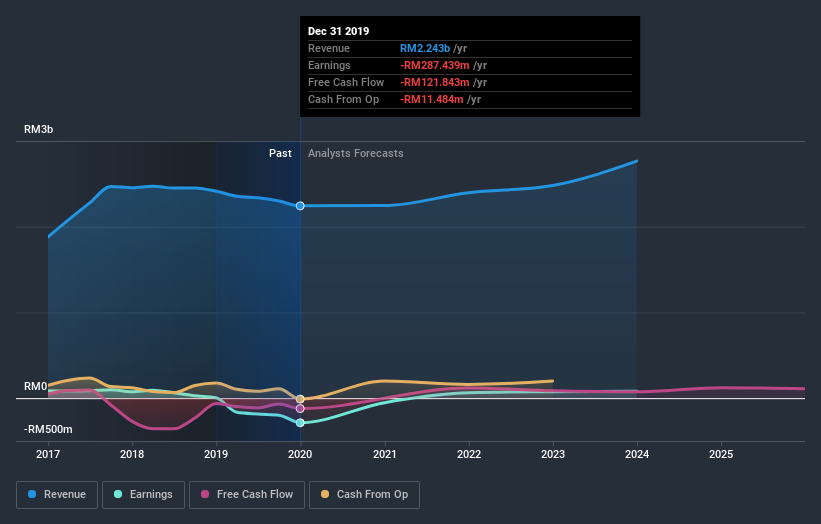

See our latest analysis for Pos Malaysia Berhad

Taking into account the latest results, the consensus forecast from Pos Malaysia Berhad's three analysts is for revenues of RM2.40b in 2021, which would reflect a modest 6.8% improvement in sales compared to the last 12 months. Pos Malaysia Berhad is also expected to turn profitable, with statutory earnings of RM0.09 per share. In the lead-up to this report, the analysts had been modelling revenues of RM2.57b and earnings per share (EPS) of RM0.065 in 2021. While revenue forecasts have been revised downwards, the analysts look to have become more optimistic on the company's cost base, given the great increase in to the earnings per share numbers.

The analysts have cut their price target 8.6% to RM1.09per share, suggesting that the declining revenue was a more crucial indicator than the expected improvement in earnings. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Pos Malaysia Berhad, with the most bullish analyst valuing it at RM1.40 and the most bearish at RM0.93 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. For example, we noticed that Pos Malaysia Berhad's rate of growth is expected to accelerate meaningfully, with revenues forecast to grow 6.8%, well above its historical decline of 7.0% a year over the past year. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 13% per year. So although Pos Malaysia Berhad's revenue growth is expected to improve, it is still expected to grow slower than the industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Pos Malaysia Berhad's earnings potential next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. Yet - earnings are more important to the intrinsic value of the business. Furthermore, the analysts also cut their price targets, suggesting that the latest news has led to greater pessimism about the intrinsic value of the business.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Pos Malaysia Berhad going out to 2023, and you can see them free on our platform here..

You still need to take note of risks, for example - Pos Malaysia Berhad has 2 warning signs (and 1 which is significant) we think you should know about.

If you’re looking to trade Pos Malaysia Berhad, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

If you're looking to trade Pos Malaysia Berhad, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:POS

Pos Malaysia Berhad

Provides postal and parcel services in Malaysia, Thailand, and internationally.

Fair value with mediocre balance sheet.