- Malaysia

- /

- Infrastructure

- /

- KLSE:BIPORT

Does Bintulu Port Holdings Berhad (KLSE:BIPORT) Have A Healthy Balance Sheet?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Bintulu Port Holdings Berhad (KLSE:BIPORT) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Bintulu Port Holdings Berhad

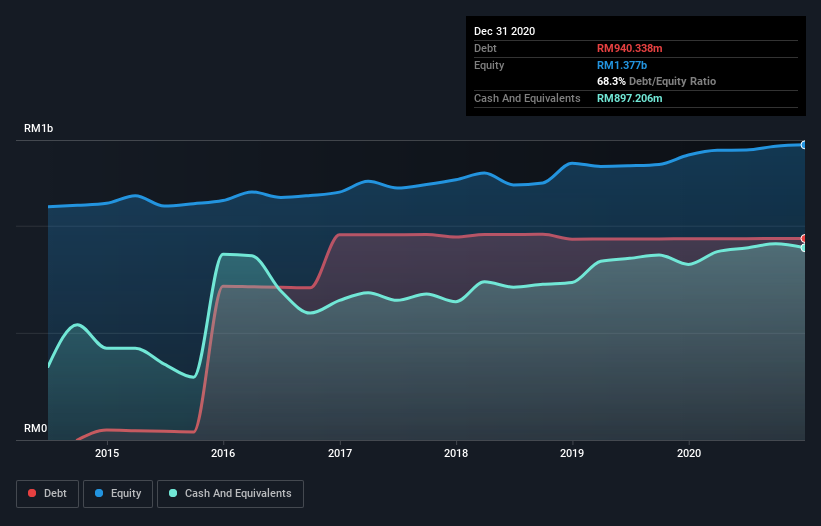

What Is Bintulu Port Holdings Berhad's Debt?

As you can see below, Bintulu Port Holdings Berhad had RM940.3m of debt, at December 2020, which is about the same as the year before. You can click the chart for greater detail. However, it also had RM897.2m in cash, and so its net debt is RM43.1m.

How Healthy Is Bintulu Port Holdings Berhad's Balance Sheet?

According to the last reported balance sheet, Bintulu Port Holdings Berhad had liabilities of RM232.0m due within 12 months, and liabilities of RM1.34b due beyond 12 months. Offsetting this, it had RM897.2m in cash and RM62.2m in receivables that were due within 12 months. So its liabilities total RM616.3m more than the combination of its cash and short-term receivables.

Bintulu Port Holdings Berhad has a market capitalization of RM1.98b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Bintulu Port Holdings Berhad has net debt of just 0.12 times EBITDA, indicating that it is certainly not a reckless borrower. And it boasts interest cover of 8.0 times, which is more than adequate. The modesty of its debt load may become crucial for Bintulu Port Holdings Berhad if management cannot prevent a repeat of the 22% cut to EBIT over the last year. When it comes to paying off debt, falling earnings are no more useful than sugary sodas are for your health. There's no doubt that we learn most about debt from the balance sheet. But it is Bintulu Port Holdings Berhad's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Happily for any shareholders, Bintulu Port Holdings Berhad actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Based on what we've seen Bintulu Port Holdings Berhad is not finding it easy, given its EBIT growth rate, but the other factors we considered give us cause to be optimistic. In particular, we are dazzled with its conversion of EBIT to free cash flow. It's also worth noting that Bintulu Port Holdings Berhad is in the Infrastructure industry, which is often considered to be quite defensive. Considering this range of data points, we think Bintulu Port Holdings Berhad is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 3 warning signs with Bintulu Port Holdings Berhad (at least 1 which shouldn't be ignored) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

When trading Bintulu Port Holdings Berhad or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Bintulu Port Holdings Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:BIPORT

Bintulu Port Holdings Berhad

An investment holding company, operates in port operator business in Malaysia and Brunei.

Flawless balance sheet with solid track record.