Despite delivering investors losses of 19% over the past 3 years, Kronologi Asia Berhad (KLSE:KRONO) has been growing its earnings

While it may not be enough for some shareholders, we think it is good to see the Kronologi Asia Berhad (KLSE:KRONO) share price up 26% in a single quarter. But that doesn't help the fact that the three year return is less impressive. Truth be told the share price declined 19% in three years and that return, Dear Reader, falls short of what you could have got from passive investing with an index fund.

The recent uptick of 14% could be a positive sign of things to come, so let's take a look at historical fundamentals.

View our latest analysis for Kronologi Asia Berhad

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

Although the share price is down over three years, Kronologi Asia Berhad actually managed to grow EPS by 54% per year in that time. This is quite a puzzle, and suggests there might be something temporarily buoying the share price. Alternatively, growth expectations may have been unreasonable in the past.

It's worth taking a look at other metrics, because the EPS growth doesn't seem to match with the falling share price.

We note that, in three years, revenue has actually grown at a 6.4% annual rate, so that doesn't seem to be a reason to sell shares. It's probably worth investigating Kronologi Asia Berhad further; while we may be missing something on this analysis, there might also be an opportunity.

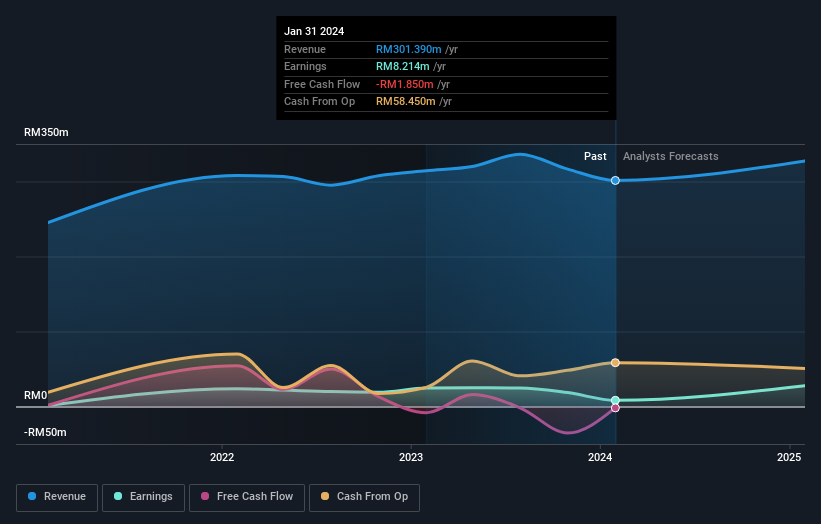

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

It's probably worth noting that the CEO is paid less than the median at similar sized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. You can see what analysts are predicting for Kronologi Asia Berhad in this interactive graph of future profit estimates.

A Different Perspective

Kronologi Asia Berhad shareholders gained a total return of 2.1% during the year. But that was short of the market average. On the bright side, that's still a gain, and it is certainly better than the yearly loss of about 0.5% endured over half a decade. It could well be that the business is stabilizing. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. For instance, we've identified 2 warning signs for Kronologi Asia Berhad that you should be aware of.

If you are like me, then you will not want to miss this free list of undervalued small caps that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Malaysian exchanges.

If you're looking to trade Kronologi Asia Berhad, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kronologi Asia Berhad might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:KRONO

Kronologi Asia Berhad

An investment holding company, provides cloud and hybrid as-a-service, and enterprise data management infrastructure technology (EDM IT) solutions in Malaysia, Singapore, China, the Philippines, India, Hong Kong, Taiwan, and internationally.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives