Advertisement

- Malaysia

- /

- Semiconductors

- /

- KLSE:VITROX

Analysts Just Made A Significant Upgrade To Their ViTrox Corporation Berhad (KLSE:VITROX) Forecasts

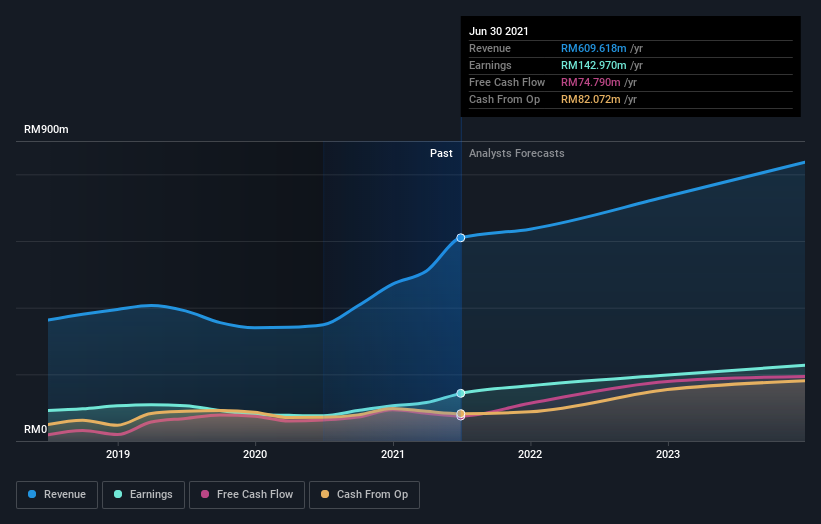

ViTrox Corporation Berhad (KLSE:VITROX) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year's forecasts. The analysts greatly increased their revenue estimates, suggesting a stark improvement in business fundamentals. ViTrox Corporation Berhad has also found favour with investors, with the stock up a noteworthy 14% to RM18.96 over the past week. It will be interesting to see if today's upgrade is enough to propel the stock even higher.

Following the upgrade, the latest consensus from ViTrox Corporation Berhad's nine analysts is for revenues of RM635m in 2021, which would reflect an okay 4.2% improvement in sales compared to the last 12 months. Per-share earnings are expected to step up 16% to RM0.35. Prior to this update, the analysts had been forecasting revenues of RM572m and earnings per share (EPS) of RM0.31 in 2021. There has definitely been an improvement in perception recently, with the analysts substantially increasing both their earnings and revenue estimates.

Check out our latest analysis for ViTrox Corporation Berhad

With these upgrades, we're not surprised to see that the analysts have lifted their price target 15% to RM18.38 per share. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values ViTrox Corporation Berhad at RM23.28 per share, while the most bearish prices it at RM11.20. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that ViTrox Corporation Berhad's revenue growth is expected to slow, with the forecast 5.7% annualised growth rate until the end of 2021 being well below the historical 16% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 17% per year. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than ViTrox Corporation Berhad.

The Bottom Line

The biggest takeaway for us from these new estimates is that analysts upgraded their earnings per share estimates, with improved earnings power expected for this year. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. With a serious upgrade to expectations and a rising price target, it might be time to take another look at ViTrox Corporation Berhad.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple ViTrox Corporation Berhad analysts - going out to 2023, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About KLSE:VITROX

ViTrox Corporation Berhad

An investment holding company, designs, manufactures, and sells automated vision inspection equipment and system-on-chip embedded electronics devices for the semiconductor and electronics packaging industries worldwide.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor