Advertisement

- Malaysia

- /

- Metals and Mining

- /

- KLSE:PMETAL

Press Metal Aluminium Holdings Berhad's (KLSE:PMETAL) Shareholders Might Be Looking For Exit

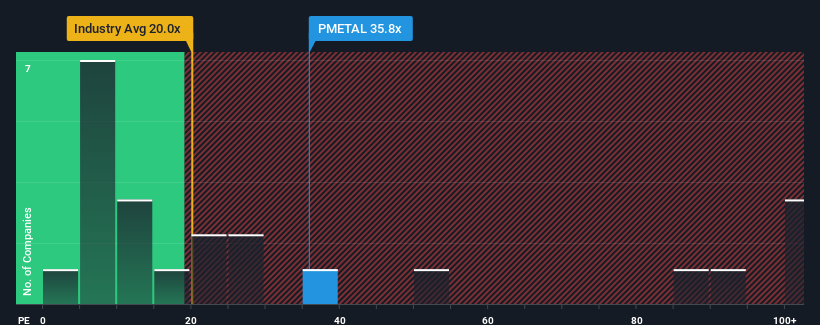

When close to half the companies in Malaysia have price-to-earnings ratios (or "P/E's") below 16x, you may consider Press Metal Aluminium Holdings Berhad (KLSE:PMETAL) as a stock to avoid entirely with its 35.8x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Press Metal Aluminium Holdings Berhad could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Press Metal Aluminium Holdings Berhad

How Is Press Metal Aluminium Holdings Berhad's Growth Trending?

The only time you'd be truly comfortable seeing a P/E as steep as Press Metal Aluminium Holdings Berhad's is when the company's growth is on track to outshine the market decidedly.

Retrospectively, the last year delivered a frustrating 14% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 159% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Turning to the outlook, the next three years should generate growth of 13% each year as estimated by the twelve analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 12% per annum, which is not materially different.

With this information, we find it interesting that Press Metal Aluminium Holdings Berhad is trading at a high P/E compared to the market. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. These shareholders may be setting themselves up for disappointment if the P/E falls to levels more in line with the growth outlook.

The Bottom Line On Press Metal Aluminium Holdings Berhad's P/E

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Press Metal Aluminium Holdings Berhad's analyst forecasts revealed that its market-matching earnings outlook isn't impacting its high P/E as much as we would have predicted. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. Unless these conditions improve, it's challenging to accept these prices as being reasonable.

It is also worth noting that we have found 1 warning sign for Press Metal Aluminium Holdings Berhad that you need to take into consideration.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:PMETAL

Press Metal Aluminium Holdings Berhad

Engages in manufacturing and trading of aluminum, and smelting and extrusion products in Malaysia, other Asian countries, Europe, the Oceania, Europe, and internationally.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor