- Malaysia

- /

- Metals and Mining

- /

- KLSE:MASTEEL

Investors Don't See Light At End Of Malaysia Steel Works (KL) Bhd.'s (KLSE:MASTEEL) Tunnel And Push Stock Down 25%

Malaysia Steel Works (KL) Bhd. (KLSE:MASTEEL) shares have had a horrible month, losing 25% after a relatively good period beforehand. The recent drop has obliterated the annual return, with the share price now down 6.1% over that longer period.

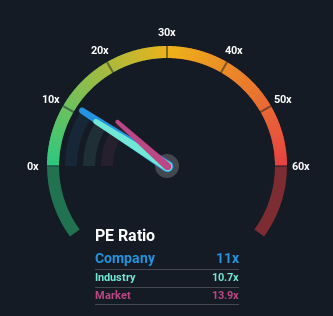

After such a large drop in price, Malaysia Steel Works (KL) Bhd may be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 11x, since almost half of all companies in Malaysia have P/E ratios greater than 14x and even P/E's higher than 25x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

For instance, Malaysia Steel Works (KL) Bhd's receding earnings in recent times would have to be some food for thought. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

See our latest analysis for Malaysia Steel Works (KL) Bhd

What Are Growth Metrics Telling Us About The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Malaysia Steel Works (KL) Bhd's to be considered reasonable.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 41%. Unfortunately, that's brought it right back to where it started three years ago with EPS growth being virtually non-existent overall during that time. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Comparing that to the market, which is predicted to deliver 11% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

With this information, we can see why Malaysia Steel Works (KL) Bhd is trading at a P/E lower than the market. It seems most investors are expecting to see the recent limited growth rates continue into the future and are only willing to pay a reduced amount for the stock.

The Final Word

The softening of Malaysia Steel Works (KL) Bhd's shares means its P/E is now sitting at a pretty low level. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Malaysia Steel Works (KL) Bhd revealed its three-year earnings trends are contributing to its low P/E, given they look worse than current market expectations. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. If recent medium-term earnings trends continue, it's hard to see the share price rising strongly in the near future under these circumstances.

You need to take note of risks, for example - Malaysia Steel Works (KL) Bhd has 4 warning signs (and 2 which can't be ignored) we think you should know about.

Of course, you might also be able to find a better stock than Malaysia Steel Works (KL) Bhd. So you may wish to see this free collection of other companies that sit on P/E's below 20x and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:MASTEEL

Malaysia Steel Works (KL) Bhd

Manufactures and markets tensile steel bars, mild steel bars, and prime steel billets for the construction and infrastructure sectors in Malaysia and internationally.

Solid track record with mediocre balance sheet.