Advertisement

Box-Pak (Malaysia) Bhd (KLSE:BOXPAK) Is Doing The Right Things To Multiply Its Share Price

What trends should we look for it we want to identify stocks that can multiply in value over the long term? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. Speaking of which, we noticed some great changes in Box-Pak (Malaysia) Bhd's (KLSE:BOXPAK) returns on capital, so let's have a look.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for Box-Pak (Malaysia) Bhd:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

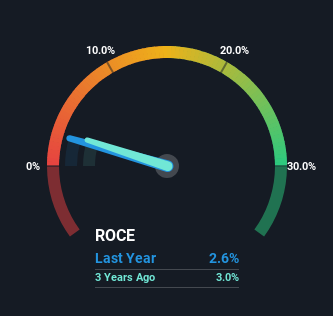

0.026 = RM5.7m ÷ (RM502m - RM285m) (Based on the trailing twelve months to March 2023).

Thus, Box-Pak (Malaysia) Bhd has an ROCE of 2.6%. Ultimately, that's a low return and it under-performs the Packaging industry average of 12%.

See our latest analysis for Box-Pak (Malaysia) Bhd

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of Box-Pak (Malaysia) Bhd, check out these free graphs here.

So How Is Box-Pak (Malaysia) Bhd's ROCE Trending?

We're delighted to see that Box-Pak (Malaysia) Bhd is reaping rewards from its investments and has now broken into profitability. Historically the company was generating losses but as we can see from the latest figures referenced above, they're now earning 2.6% on their capital employed. In regards to capital employed, Box-Pak (Malaysia) Bhd is using 26% less capital than it was five years ago, which on the surface, can indicate that the business has become more efficient at generating these returns. Box-Pak (Malaysia) Bhd could be selling under-performing assets since the ROCE is improving.

On a side note, Box-Pak (Malaysia) Bhd's current liabilities are still rather high at 57% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line On Box-Pak (Malaysia) Bhd's ROCE

In a nutshell, we're pleased to see that Box-Pak (Malaysia) Bhd has been able to generate higher returns from less capital. Astute investors may have an opportunity here because the stock has declined 21% in the last five years. So researching this company further and determining whether or not these trends will continue seems justified.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 3 warning signs for Box-Pak (Malaysia) Bhd (of which 2 can't be ignored!) that you should know about.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

Valuation is complex, but we're here to simplify it.

Discover if Box-Pak (Malaysia) Bhd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About KLSE:BOXPAK

Box-Pak (Malaysia) Bhd

An investment holding company, engages in the manufacture and distribution of paper boxes, cartons, general papers, and board printing products in Malaysia, Vietnam, and Myanmar.

Low and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor